Table of Contents

108

5 min

25.06.2026

Management Accounting for an Agency: The Per-Client View That Changes Everything

Julia Polinyak

Financial expert at Finmap

"I knew our revenue per client. I knew our headline retainer rates. And when our biggest client asked for a 12% discount, I had no real basis to decide whether to say yes."

A founder running a small marketing/PR agency described the conversation that broke her decision-making. Her largest client — ₴84K/month retainer, three years of relationship — asked for a 12% discount in renewal negotiations. He framed it as routine.

She had 48 hours to decide. She had no real numbers to base the decision on.

She knew her agency was profitable. She knew this client was important. She didn't know: how much of her team's time this client actually consumed, what the effective hourly rate was after accommodating his Friday-evening urgent requests, what the contribution margin was after the deliverables he'd added beyond the original scope, what the cash impact of losing him would be, or whether two of her other clients were more profitable per hour and could fill the gap if she walked.

She accepted the discount. A year later, with proper management accounting in place, she realized he had been her lowest-margin retainer client — and the discount turned him into a small loss. By then, the discount was a year of commitment.

This article is about what management accounting looks like for a creative, marketing, or PR agency — and the per-client view that makes renewal conversations and pricing decisions structured rather than instinctive.

The Paradox: Retainer Revenue Hides More Than It Reveals

Agency owners watch retainer revenue carefully — it's predictable, it's the foundation of cash flow, it's how the agency talks about itself externally. But aggregate retainer revenue hides the variation that matters.

- One ₴35K retainer might consume 22 team hours per month (effective rate ₴1,590/hr — healthy)

- Another ₴35K retainer might consume 51 team hours per month (effective rate ₴686/hr — silently underwater)

- The two clients look identical on the P&L and very different in reality

Aggregate retainer revenue tells you the agency is funded. Per-client management accounting tells you which retainers are funding the agency and which are quietly bleeding it. Renewal conversations, pricing decisions, and team allocation all depend on knowing the difference.

The general framework is in the anchor article → Management Accounting Explained.

The Four Agency-Specific Metrics

Metric two — Scope creep ratio. Hours delivered vs hours originally scoped. Sustainable agencies run at 100–110% (small overruns absorbed). Agencies running at 130%+ on multiple clients are giving away their margin in deliverables nobody asked them to repay for. Tracked monthly per client, this metric is the clearest signal of whose scope needs renegotiation.

Metric three — Contribution margin per client. Revenue minus fully-loaded delivery cost (team time at loaded rates plus direct subcontractor/tool costs) before allocated overhead. The single most important number for client mix decisions. Sort clients by this, top to bottom: the bottom three are the renegotiation queue.

Metric four — Retainer health score. A composite combining effective rate, scope creep, payment timeliness, and relationship indicators. Useful as a single owner-facing signal during renewal season.

How Those Metrics Change Renewal and Pricing Decisions

When the four metrics exist, the conversation with the 12% discount client transforms.

Without the metrics: "He's important. We can absorb 12%. Probably."

With the metrics: "His effective rate is already 18% below threshold. Scope creep is at 142%. His contribution margin is third from the bottom across our 11 clients. A 12% discount would put him into negative contribution territory. We have two options: (a) accept the discount only if we tighten scope and reduce delivered hours by 25%; (b) decline the discount, accept the risk he walks. Modeled cash impact of him walking: minus ₴84K for one quarter, recovered by mid-Q2 through pipeline."

The decision is now structured. It can still go either way — but it's grounded in what the agency actually knows rather than what it fears.

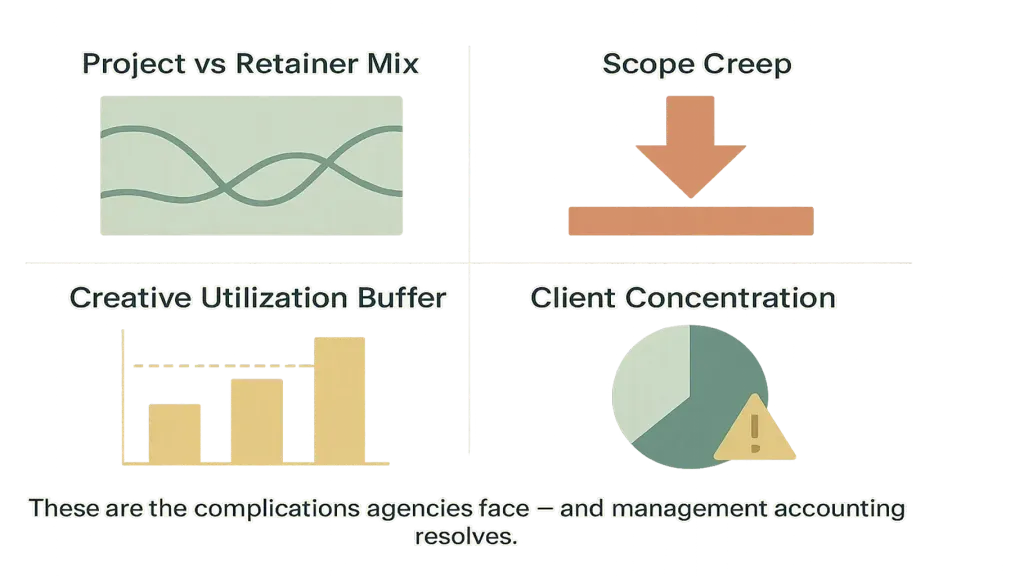

Agency-Specific Complications

Agencies have a few complications that make management accounting harder than for product businesses — and more valuable when done.

Scope creep. The silent margin killer of every agency. Not always bad — sometimes scope creep is how relationships deepen. Tracked over time, it reveals which clients respect boundaries and which don't.

Team utilization (with creative buffer). Unlike consulting or dev, creative agencies need unbillable time for the work to be good — thinking, exploring, the conference, the half-day someone spends watching ten ads from a category. Healthy creative utilization runs 55–65% (lower than dev agencies). Push above 75% sustainably and quality drops.

Client concentration. Agencies trend toward concentration because relationships compound. A single client at 30%+ of revenue is both a strength (deep account knowledge) and a risk (their churn could halve the agency overnight). Management accounting surfaces this risk explicitly.

How to Install Management Accounting in 90 Days

Phase 1 — Foundation (weeks 1–4). Install time tracking that distinguishes billable, scope, unscoped, and unbillable creative time. Map every client retainer's scope. Note disconnects between scope and reality.

Phase 2 — Mapping (weeks 5–8). Calculate per-client effective rate, scope creep, contribution margin for the previous quarter. Build the retainer health composite.

Phase 3 — Decision integration (weeks 9–12). Identify the bottom three clients by contribution margin. For each: one rate adjustment, one scope tightening, or one graceful exit. The pattern from these decisions trains future renewals.

📌 See how management accounting looks for a creative or marketing agency — per-client effective rate, scope creep tracking, contribution margin, retainer health. Book a 20-minute Finmap demo. Book a Finmap demo →

Topic foundation: Management Accounting Explained: What It Is and Why Owners Need It

Share valuable content — become a source of insights

Frequently Asked Questions

My agency has only 3 retainers. Is per-client accounting overkill?

The fewer retainers, the more each one matters. With 3, you have no diversification — one bad retainer is 33% of your business. Per-client visibility is essential.

My team won't track time accurately for creative work.

Reasonable concern. Two solutions: track time in larger blocks (4-hour minimum), and frame it as "what work happened" rather than "what did you do every minute." Quality of data matters more than precision.

Can we just look at revenue per client and approximate?

You can. You'll miss the scope creep and effective rate signals — which are usually where margin is bleeding.

Should I share contribution margin with the team?

Per-client margin: usually not. Aggregate health signals and "which clients are healthy": usually yes. Team responds to clarity about where the agency stands.

What if a client asks for a discount during renewal?

With the metrics in place, the conversation becomes structured. Without them, it's anxiety with a calculator. Article #5 → financial model that supports renewal scenarios.

How does this connect to bookkeeping?

Bookkeeping handles invoices, tax, compliance. Management accounting sits on top — using time tracking + accounting to produce the four agency-specific metrics. Article #2 →

Any questions left?

We are ready to answer them.

Finmap support