Table of Contents

150

11 min

25.06.2026

Management Accounting Explained: What It Is and Why Owners Need It

Sergiy Shuldik

Financial Expert at Finmap

"I get a beautiful monthly report from my accountant. It's accurate. It's professional. And it doesn't help me make a single decision."

Most small business owners have one of three relationships with their financial information.

The first: no reports. They look at the bank balance and that's the system.

The second — by far the most common: bookkeeping only. An accountant sends a monthly P&L and tax returns. The owner reads briefly, signs, files. The reports are accurate. They are also unactionable. No decisions get made differently because of them.

The third: management accounting. The owner has a structured set of reports designed to answer specific decision-questions. Where to price. When to hire. Which clients are actually profitable. What the next 90 days look like.

The vast majority of growing businesses sit firmly in the second category. They have an accountant. They have monthly reports. They believe they have financial visibility. They don't — they have historical record-keeping that's been quietly confused with decision support.

This article is about that confusion. What management accounting actually is (and isn't). Why owners specifically need it. And what changes the moment it's installed.

What Management Accounting Actually Is

A definition free of jargon:

Management accounting is the practice of organizing a business's financial information so the owner can make better operating, pricing, and strategic decisions.

Three things matter in that sentence.

"For the owner." Not for the tax authority. Not for the bank. Not for the external auditor. Management accounting is the only financial discipline whose primary audience is the person running the business. Everything else — bookkeeping, financial accounting, tax accounting — serves external requirements first and the owner's decisions only incidentally.

"Decisions." The entire purpose of the practice. A management accounting report exists to answer a specific question. Which clients are most profitable per hour of team time? Can we afford to hire one more designer in Q3? Should we raise our retainer fee? If a report doesn't help answer at least one of these kinds of questions, it isn't management accounting — it's filing.

"Organizing information." The work is structural, not just numerical. The same raw transactions can be organized to tell you very different things depending on how you slice them. A ₴4 million business looked at as one monolithic P&L tells you almost nothing. The same business sliced by client, by service line, by month, by margin — tells you everything.

How It Differs From Bookkeeping (the Short Version)

Bookkeeping is the accurate recording of every transaction that happened. It exists to satisfy tax authorities, banks, and external auditors. It's historical, regulated, and backward-looking. It's done by an accountant.

Management accounting is the organization of that data so the owner can decide what to do next. It's present and future-tense, internal, and decision-oriented. It's done by the owner — sometimes with the accountant, sometimes with an external advisor, sometimes alone.

The two practices need each other. Bookkeeping without management accounting produces accurate records nobody uses to make decisions. Management accounting without clean bookkeeping is built on sand.

A deeper comparison — what each one does, what each can't do, and where they overlap — is the subject of the next article in this series: The Difference Between Bookkeeping and Management Accounting.

For now, the one-line summary: bookkeeping tells you what happened. Management accounting tells you what to do about it.

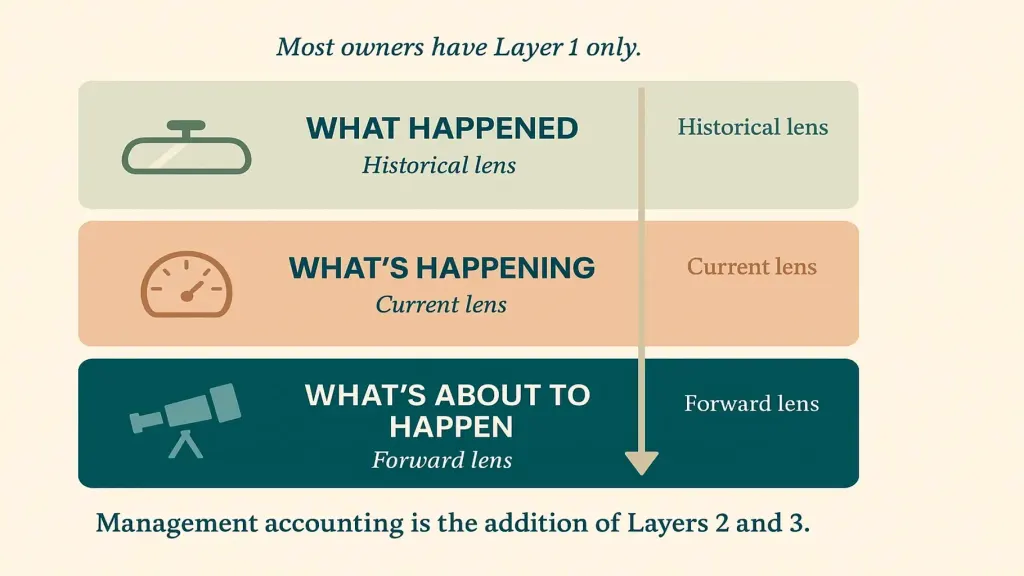

The Three Temporal Layers of Management Accounting

A complete management accounting practice has three layers, organized by time horizon.

Layer 2 — What's happening (current lens). Today's cash position across all accounts. Open receivables and their age. Current month's run-rate vs. forecast. Where the business stands right now, this minute, with enough resolution to act on without waiting for the next monthly close.

Layer 3 — What's about to happen (forward lens). The 14- to 90-day payment calendar. The 12-month financial model. Scenarios for major decisions ("if we hire two people, what does Q4 look like?"). The forward lens is where strategic decisions actually get made.

Most owners have Layer 1 only — from their bookkeeping. The shift to real management accounting is the addition of Layers 2 and 3.

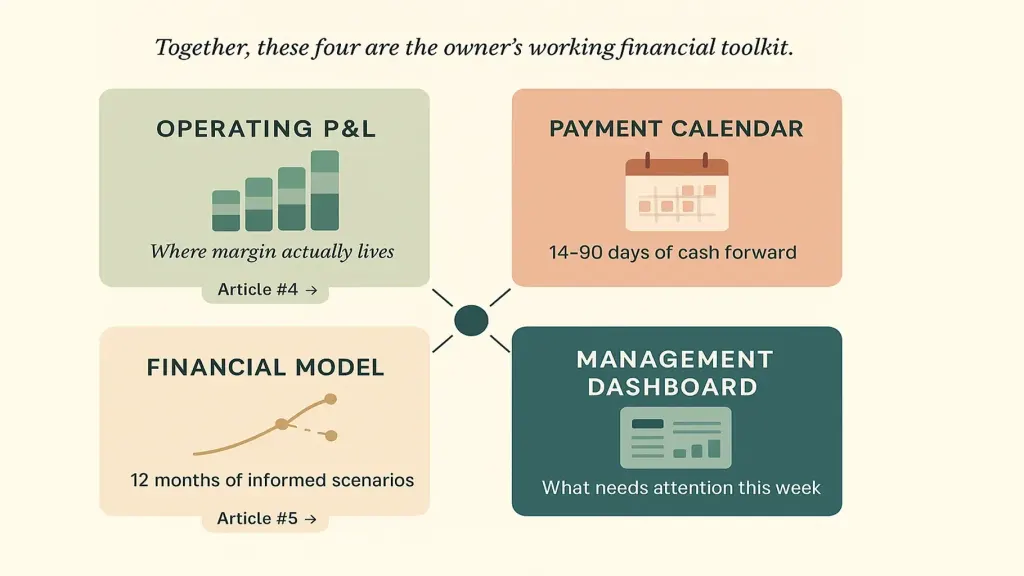

The Four Core Artifacts

In practice, management accounting produces four documents (or dashboards) that an owner uses regularly.

Two — the cash flow / payment calendar. The 14- to 90-day view of inflows, outflows, and projected balance. This is where most cash gaps get caught before they become crises.

Three — the financial model. A 12-month forward-looking model showing how decisions today affect cash, profit, and headcount over the year. Not perfect predictions — informed scenarios. Article #5 in the series — Financial Model for a Small Business — goes deep on this.

Four — the management dashboard. A single one-page summary the owner reviews weekly: cash position, runway, AR aging, contribution margin trends, key client metrics. The dashboard exists so the owner doesn't have to dig through four separate documents — it surfaces what needs attention this week.

Each artifact answers a different question. Together, they make up the owner's working financial toolkit.

What Changes When Management Accounting Is in Place

The bookkeeping-only owner runs the business by feel, instinct, and reactive response. The management-accounting owner runs it by structured, informed decision-making.

The shift shows up in specific places:

- Pricing. Instead of "we charge ₴X because we always have," pricing becomes data-driven: contribution margin per hour, per client type, per service line — informing where rates should move.

- Hiring. Instead of "we feel we can afford one more," hiring becomes modeled: the cash impact, the timeline to break-even on the new hire, the runway implication.

- Client mix. Instead of "all clients are roughly the same," client mix becomes managed: dropping unprofitable clients, doubling down on profitable ones.

- Cash decisions. Instead of reactive panic about supplier payments, cash decisions become proactive — early-pay discounts, timing negotiations, planned buffer accumulation.

- Strategic decisions. Instead of "let's see how it goes," major decisions get scenario-modeled before they're committed.

The accountant's monthly report — accurate but unactionable — gets replaced by a small system that produces answers, not just records. The owner stops asking "did we do well?" and starts asking "what should we do?"

How to Start

Three stages, sequential.

Stage 1 — Foundation (1–2 weeks). Build the account map: every place money lives — operating, tax reserve, strategic reserve, FX accounts, petty cash, payment processor floats. Get bookkeeping clean: every transaction categorized correctly, with the right level of detail (by client and by service line, not just "income"). Produce a baseline operating P&L for the previous quarter — segmented. This is the platform everything else builds on.

Stage 2 — Layers (2–4 weeks). Add the payment calendar (the operational forward view). Add a basic 12-month financial model (the strategic forward view). Set up the management dashboard (the regular review surface). By the end of this stage, you should be able to answer "what's our cash runway?" in under 30 seconds, and "which client is our most profitable per team hour?" without doing math on the spot.

Stage 3 — Integration (ongoing). Automate where possible — bank-feed integration, scheduled report generation, recurring transaction categorization. Install the review cadence: weekly 30-minute review, monthly 90-minute close, quarterly strategic session. Article #3 in the series — What a Financial Management Platform Is — covers the tooling that makes Stage 3 sustainable.

By the end of Stage 3, management accounting is no longer a project. It's just how the business runs.

📌 See what management accounting looks like as a working system — not as a concept. Book a 20-minute Finmap demo. We'll show you the four core artifacts on real example data, walk through how it works for a business like yours, and answer "where would I start with my numbers?" before you go. Book a Finmap demo →

Read also

- Bookkeeping vs management accounting: the difference

- Accounting vs financial management explained

- What is a financial management platform?

In this topic

- Bookkeeping vs Management Accounting: The Two Different Languages of Business Finance

- Accounting vs Financial Management: Why You Need Both?

- What a Financial Management Platform Is — And Why It's Not Just Accounting Software in a Browser

- How to Choose Financial Management Software: Excel, 1C, or Finmap?

- Management Accounting for an Agency: The Per-Client View That Changes Everything

- Management Accounting for an IT Agency: The Three Numbers That Tell You Everything

Share valuable content — become a source of insights

Frequently Asked Questions

My accountant says they do "management accounting." Is that the same thing?

Sometimes yes, often no. Many accountants offer "management reporting" as an add-on — usually a more frequent or more segmented version of the standard P&L. That's helpful, but it's only Layer 1 (historical). True management accounting includes Layers 2 and 3 (present and forward), which most accountants don't produce because they require ongoing engagement with the business's operational reality, not just transaction recording.

Do I need a different person to do management accounting than my bookkeeper?

Not necessarily, but the skill set is different. Bookkeeping is recording and reporting. Management accounting is interpretation and decision support. Some accountants do both well. Some don't. Article #8 in this series — Outsourced Finance Director: When You Need One — discusses when to engage a higher-tier finance person specifically for management-accounting work.

At what business size does management accounting become essential?

For most service businesses: when revenue crosses ₴2–3 million annual or when you have three or more employees. Before that, gut feeling and bookkeeping can carry you. After that, the cost of not having management accounting compounds quickly. Article #9 — Financial Management for a Small Business — addresses this size threshold directly.

Can I do this in spreadsheets?

The first iteration — yes. For six to twelve months, a structured Google Sheets setup can produce real management accounting if the owner is disciplined. After that, most owners switch to a platform because the manual maintenance becomes the bottleneck. Article #3 — What a Financial Management Platform Is — explains the tooling shift.

My business is too small. Should I wait?

The earlier you install management accounting, the easier it stays. A ₴1 million business adding the basics today builds the habit; a ₴10 million business trying to add it from scratch struggles with embedded complexity that's already there. Start small — even an operating P&L segmented by client is a real beginning.

Where do I start tomorrow?

The single highest-leverage first step: produce an operating P&L for the last three months, segmented by client and service line. That one document, even rough, will already start revealing decisions you didn't know you could make. From there, the payment calendar is the natural next step.

Any questions left?

We are ready to answer them.

Finmap support