Table of Contents

175

12 min

25.06.2026

Bookkeeping vs Management Accounting: The Two Different Languages of Business Finance

Sergiy Shuldik

Financial Expert at Finmap

"I asked my accountant three questions in one meeting. She answered all three — accurately, calmly, professionally. And none of the answers helped me decide what to do."

A marketing-studio founder I'll call our anchor character ran her quarterly review with her accountant last spring. She had prepared three questions.

Question one: "Of our six retainer clients, which two are most profitable per hour of team time?"

The accountant's answer, after some calculation: "I can show you revenue per client. We don't track team hours by client in the books, so per-hour profitability isn't something I can produce from this data."

Question two: "If we hire one more designer in June, what does our cash look like at the end of Q3?"

The accountant: "I can show you what cash looked like at the end of last Q3. Projecting forward isn't really what these books are built for."

Question three: "Should we raise our retainer rate from ₴35K to ₴42K?"

The accountant: "That's a business decision. I can show you what our margins were at the old rate, but the pricing question is yours."

Each answer was accurate. Each was professional. None of them helped her decide what to actually do.

This is not because her accountant was bad. Her accountant was excellent at the work she was hired to do — which was bookkeeping, not management accounting. The two are different practices, serving different audiences, with different rules, and most owners confuse them because the words sound similar and the people involved often share titles.

This article is about the actual difference. Why both exist. Where each stops being useful. How owners get tripped up by the confusion. And how to set both up to work together — so that next quarterly review answers the three questions instead of dodging them.

Why This Confusion Exists — Two Different Audiences

The simplest way to understand the difference is to ask: who is the report for?

Bookkeeping serves external audiences first. The tax authority needs to know how much you earned, how much you spent, and how much tax you owe. The bank needs to know your financial health to extend a credit line. The auditor (if you have one) needs to verify everything was recorded according to standards. These audiences require accuracy, consistency, and compliance with specific rules. The owner gets the same reports as a courtesy.

Management accounting serves the owner first. The owner needs to know which clients are profitable, when cash will be tight, whether a new hire is affordable, where to set prices. These questions require segmentation, forecasting, and interpretation — things the tax authority neither wants nor needs. The accountant might benefit from these reports too, but the owner is the primary user.

When a single person — usually titled "accountant" — produces both kinds of work, the bookkeeping always gets done first (because legal deadlines exist) and the management accounting often gets skipped or done quickly (because no deadline forces it). The result is that most growing businesses have rigorous bookkeeping and almost no management accounting — and the owner doesn't notice because the bookkeeping reports look like financial visibility.

This problem — having bookkeeping confused with management accounting — is exactly what the anchor article in this series is about: Management Accounting Explained: What It Is and Why Owners Need It →

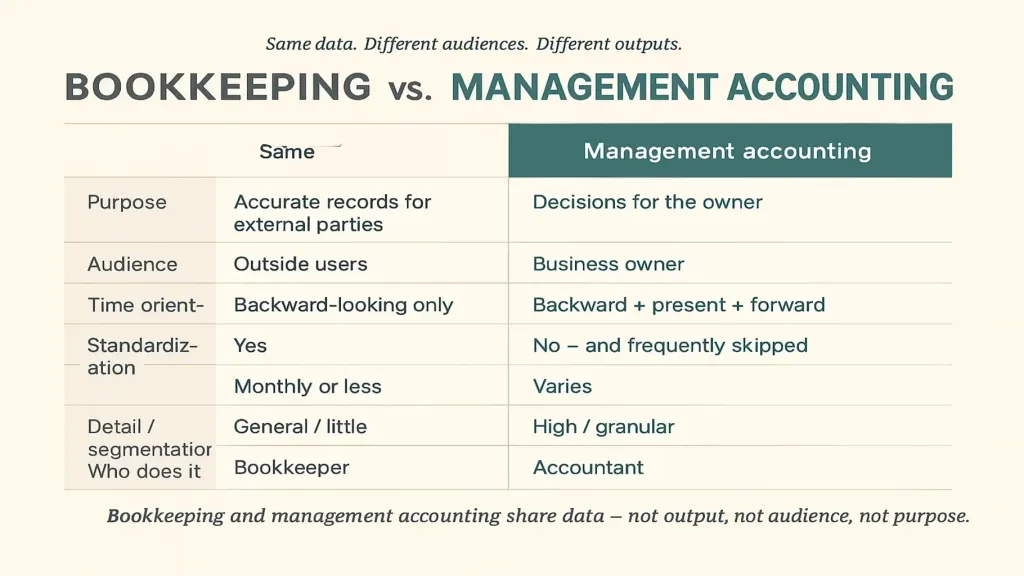

The 8-Dimension Side-by-Side Comparison

The cleanest way to see the difference is to lay both practices out across eight dimensions.

Dimension 2 — Audience. Bookkeeping: tax authority, bank, auditor, government statistics. Owner third or fourth in line. Management accounting: the owner first. Sometimes a CFO, finance advisor, or board, second.

Dimension 3 — Time orientation. Bookkeeping: purely backward-looking. What happened last week, last month, last quarter. Management accounting: backward + present + forward. What happened, what's happening, what's about to happen.

Dimension 4 — Required by law? Bookkeeping: yes. Every business above a minimal size must keep books to file taxes. Management accounting: no. It's optional in legal terms — and frequently skipped because of that.

Dimension 5 — Standardization. Bookkeeping: heavily standardized (tax codes, accounting standards, chart of accounts). Same form in every business of similar type. Management accounting: tailored to the business. A construction firm and a SaaS company use entirely different management accounting structures.

Dimension 6 — Frequency. Bookkeeping: monthly close, quarterly returns, annual reports — driven by external deadlines. Management accounting: daily cash glance, weekly review, monthly close, quarterly strategic session — driven by decision cycles.

Dimension 7 — Level of detail / segmentation. Bookkeeping: aggregated by category required for tax. "Revenue" is one line. "Cost of services" is one line. "Salaries" is one line. Management accounting: segmented by whatever the owner needs to decide. Revenue per client, cost per project, salary per role, margin per service line.

Dimension 8 — Who does it. Bookkeeping: a qualified accountant or bookkeeping firm. Regulated profession in most countries. Management accounting: the owner, often with a CFO or external finance director, sometimes with an experienced accountant who has stepped beyond their core training. Article #8 — Outsourced Finance Director: When You Need One →

These eight dimensions add up to a deceptively important conclusion: bookkeeping and management accounting share data — but they don't share output, audience, or purpose. They are different disciplines that happen to read from the same source.

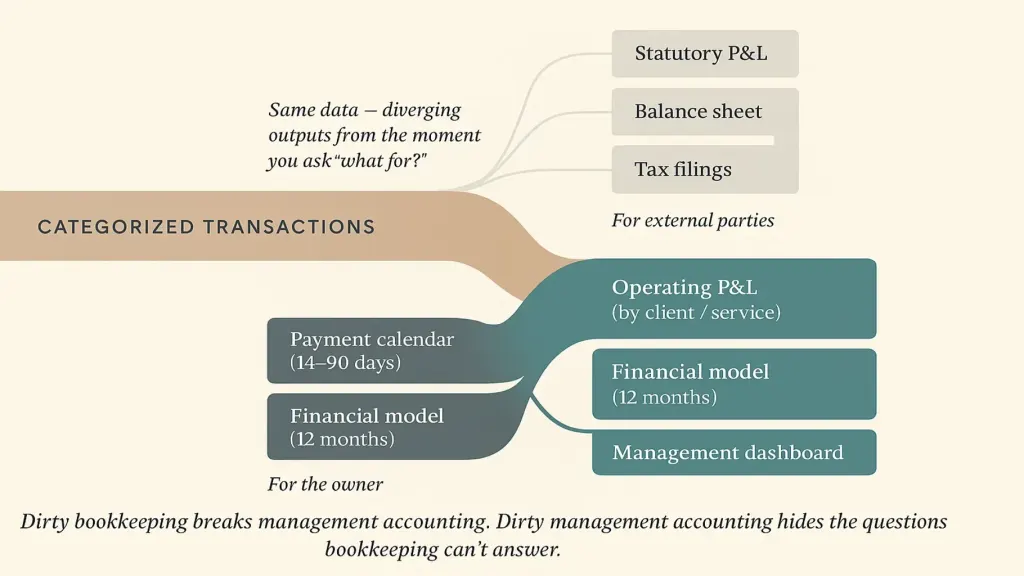

Where Bookkeeping Ends and Management Accounting Begins

It's tempting to draw a hard line — bookkeeping is "the past" and management accounting is "the present and future." In practice, the boundary is more interesting than that.

The shared territory is the categorized transaction record: every payment in and out of the business, attached to a date, a counterparty, and a category. This is what bookkeeping produces and what management accounting consumes. Both practices want this data clean, complete, and accurate.

The boundary shows up the moment you ask what to do with it.

The management accounting branch produces what the owner needs: operating P&L segmented by client and service line, payment calendar, financial model, management dashboard. Article #4 — P&L Report: How to Read It and Why It Matters → covers the operating P&L specifically; article #5 — Financial Model for a Small Business → covers the model.

Both branches need the river upstream to be clean. Dirty bookkeeping breaks management accounting — and dirty management accounting hides the questions bookkeeping can't answer.

Three Common Pitfalls Owners Fall Into

After dozens of consulting calls with owners about this exact gap, the same three traps appear over and over.

Pitfall one — assuming bookkeeping is enough. The owner signs the monthly reports, files them, feels in control of the finances. The bookkeeping is genuinely accurate. The owner can name last quarter's revenue. They can quote their tax bill. They cannot, when asked, name their most profitable client, predict next quarter's cash, or model the cost of a new hire. The gap is invisible until a decision arrives that bookkeeping can't support — and by then the decision is usually already overdue.

Pitfall two — hiring a bookkeeper expecting management accounting. The owner posts a job for "accountant" or "bookkeeper," hires the most experienced applicant, and assumes management accounting is included. Six months in, the books are immaculate and the owner still has no answers to operational questions. The bookkeeper isn't underperforming — they're producing exactly what bookkeepers produce. The owner just expected something the role doesn't include.

Pitfall three — building management accounting on broken bookkeeping. The opposite trap. The owner installs a payment calendar, a management dashboard, a forecast model — but the underlying bookkeeping is rough. Transactions are uncategorized or miscategorized. Some accounts aren't tracked. The forecasts are built on shaky historical data and produce false confidence. A management dashboard on top of poor bookkeeping is worse than no dashboard — because the owner trusts it.

The fix for all three pitfalls is the same: acknowledge that you need both disciplines, and structure who does which. Either one accountant takes on both with a clear scope (rare, but possible), or two roles split the work (a bookkeeper for compliance, an owner or external finance director for management). Either way, both must exist, both must be funded, both must communicate.

How to Set Up Both to Work Together

Bookkeeping and management accounting are different practices, but they're not adversaries. They work best when they're explicitly coordinated.

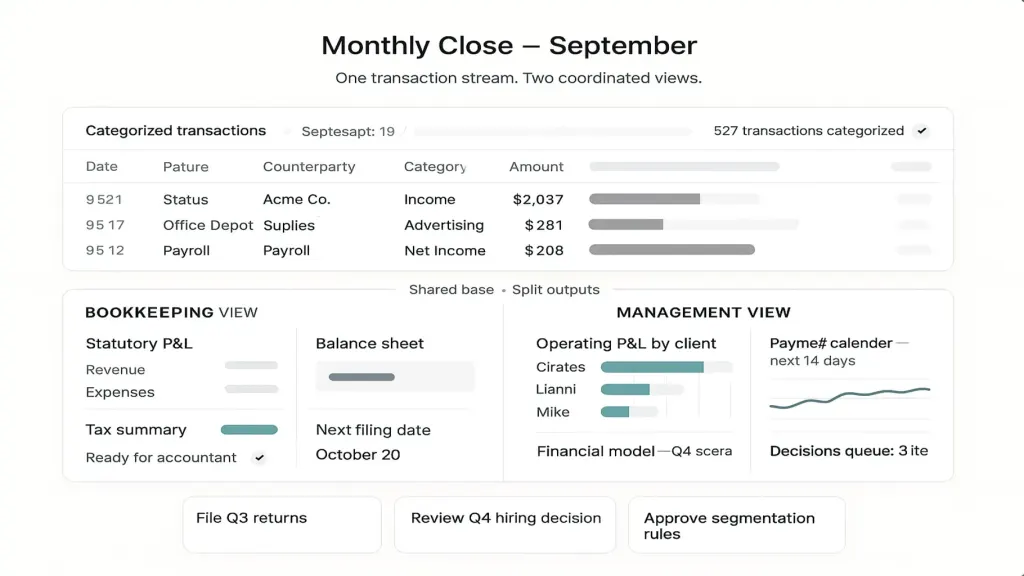

One — agree on a unified chart of accounts that serves both. Most charts of accounts are built for tax filing. They have too few categories to be useful for management ("services revenue" is one line). The fix is to design a chart that has enough segmentation for management (revenue by service line, salaries by team) while still rolling up into tax-compliant categories. The bookkeeper enters once; both reports come out cleanly.

Two — schedule a single monthly close that produces both outputs. Rather than running bookkeeping on one timeline and management accounting on a different one, treat the first week of each month as the joint close. Bookkeeping output goes to the tax filings (or holds them). Management output goes to the owner's monthly review. Same data, two views, one process.

Three — install one shared platform where possible. Spreadsheets work for the first year. After that, a platform that handles both (or integrates cleanly between bookkeeping software and management accounting software) is what makes the joint close sustainable. Article #3 — What a Financial Management Platform Is → covers the tooling side of this directly.

When set up well, the founder from the opening story now gets all three of her questions answered. Profitability per client, per hour. Forward cash projection. Pricing-change scenario. None of those answers come from bookkeeping alone — they come from management accounting built on top of clean bookkeeping. The accountant still handles the compliance. The owner (or her finance partner) handles the decisions.

📌 See bookkeeping and management accounting working together in one view — not as two separate worlds. Book a 20-minute Finmap demo. We'll show you how a single transaction stream produces both statutory outputs and management outputs, and how the joint monthly close works for a business like yours. Book a Finmap demo →

Read also

Topic foundation: Management Accounting Explained: What It Is and Why Owners Need It

Share valuable content — become a source of insights

Frequently Asked Questions

Can my current accountant do both?

Sometimes yes, often not. The skill sets are different. Bookkeeping is detail-oriented record-keeping. Management accounting is interpretive decision-support work. Some accountants enjoy both and have the bandwidth for both. Others prefer (and are better at) just the compliance side. The honest conversation to have: "Beyond the monthly close and tax filings, can you produce an operating P&L segmented by client and a 90-day cash forecast for me?" If the answer is uncertain, the second role probably needs to exist somewhere.

Do I need separate software for each?

Not necessarily. Some platforms cover both — handling the bookkeeping side of categorization, multi-account tracking, and statutory reporting, while also producing the management views (operating P&L, payment calendar, management dashboard). Spreadsheets can also bridge both for smaller businesses. Article #3 — What a Financial Management Platform Is → explains how integrated platforms work.

At what business size does the distinction matter?

For most service businesses: by ₴2 million annual revenue or three-plus employees, the distinction starts costing real decisions. Below that, the owner can often hold enough in their head to compensate. Above that, the gap between bookkeeping-only and management accounting becomes visible in monthly decisions: hires, pricing, client cuts. Article #9 — Financial Management for a Small Business → covers when management accounting becomes a must-have.

My accountant says they "do management reporting." Is that the same as management accounting?

Often partially. "Management reporting" usually means a more frequent or more segmented version of the standard P&L — useful, but only Layer 1 (historical) of the three temporal layers in real management accounting. The present and forward layers (current cash position, 90-day projections, decision scenarios) usually require additional work or a different role.

What about audited businesses — do they need both?

Especially those businesses. An audit is the most external form of bookkeeping use — auditors validate that books were kept according to standards. None of that validation answers operational questions. Audited businesses often have exemplary bookkeeping and near-zero management accounting — and their owners run on instinct despite their books being immaculate.

Where do I start tomorrow?

The single highest-leverage action: schedule a 60-minute conversation with your current accountant. Ask three operational questions (profitability per client, forward cash, hire affordability). Listen to which questions they can answer from current data, which require new work, and which they think aren't their job. Whatever they can't answer becomes your management accounting scope — either added to their work, or assigned elsewhere.

Any questions left?

We are ready to answer them.

Finmap support