Table of Contents

Home

/

Blog

/

What a Financial Management Platform Is — And Why It's Not Just Accounting Software in a Browser

199

12 min

25.06.2026

What a Financial Management Platform Is — And Why It's Not Just Accounting Software in a Browser

Sergiy Shuldik

Financial Expert at Finmap

"By year five, I had tried four different financial tools. Each one was excellent at what it was built to do. None of them did what I actually needed."

A founder running a small consulting practice walked me through her tool history one afternoon. It was a familiar story.

Year one was Excel. She built a single spreadsheet — revenue per client, expenses by category, a running balance estimate. It worked. By the end of year two, the spreadsheet had four tabs, three currencies, broken links between cells, and a deep fear of opening it.

Year three she switched to a proper bookkeeping software — 1C / QuickBooks / similar. The accountant loved it. Tax filings became easier. Monthly reports were generated automatically. But when she opened it herself, she saw screens full of journal entries, chart-of-accounts codes, and statutory reports — built for someone who knew accounting. She didn't.

Year four she added a "BI tool" on top — Power BI with custom dashboards an external consultant set up. The dashboards looked beautiful. The first month they refreshed correctly. By the third month, the underlying data structure had shifted and three charts were silently broken. By month six, she was looking at numbers she didn't trust.

Year five she stopped trying to fix the stack and asked a different question: what kind of tool was actually built to help an owner like me make decisions? The answer turned out to be a different category of software than any of the previous three — neither bookkeeping nor BI nor spreadsheet, but something that exists in the gap between them.

That category has a name. It's called a financial management platform. Most owners haven't heard the term because the tool category is younger than the others. This article is about what it is, what it does, and how it sits between the tools you've probably already tried.

The Paradox: Each Tool Was Good at Its Job

The story above contains a clue most owners miss. All four tools she tried were genuinely good at what they were built to do.

- Excel is the most flexible piece of software ever invented. It will let you build anything. It will also let you break anything.

- Bookkeeping software is designed for accountants. Its job is to keep books accurate and produce tax-compliant outputs. It does that exceedingly well.

- BI tools are designed for analysts. Their job is to slice clean data into beautiful charts. Given clean data, they do that exceedingly well.

- Spreadsheets, accounting software, and BI tools all serve specific users with specific needs.

The missing user is the owner. The owner doesn't want to build a custom spreadsheet, doesn't want to read journal entries, and doesn't want to maintain a BI tool's data pipeline. The owner wants to look at one screen and answer four questions: how much cash do I have, what's coming, what should I do this week, and what should I do this quarter? None of the existing tool categories were designed to answer those four questions directly.

A financial management platform is the category of software that exists specifically to answer them.

What a Financial Management Platform Actually Is

A definition free of marketing language:

A financial management platform is software designed specifically to help business owners and finance leaders see, decide on, and act on their company's financial state — across all accounts, in present and forward views, without requiring accounting training or technical setup work.

Three things matter in that sentence.

"Designed specifically for owners and finance leaders." Not for accountants. Not for analysts. Not for tax authorities. The primary user is the person whose decisions move the business — and the entire interface, workflow, and report structure assumes that user, not a different one.

"Across all accounts, in present and forward views." Bookkeeping software focuses on past transactions in regulated formats. A management platform aggregates everything (multiple banks, multiple currencies, payment processors, cash) and produces present (where the business stands today) and forward (what's about to happen) views. It's not just a historical record — it's a working surface for decisions.

"Without requiring accounting training or technical setup work." The killer feature isn't the dashboards or the calculations — it's the absence of barriers. A financial management platform produces management accounting outputs (operating P&L, payment calendar, financial model, dashboard) without requiring the owner to know what each of those things technically is. The four core artifacts are introduced in the anchor article — Management Accounting Explained →

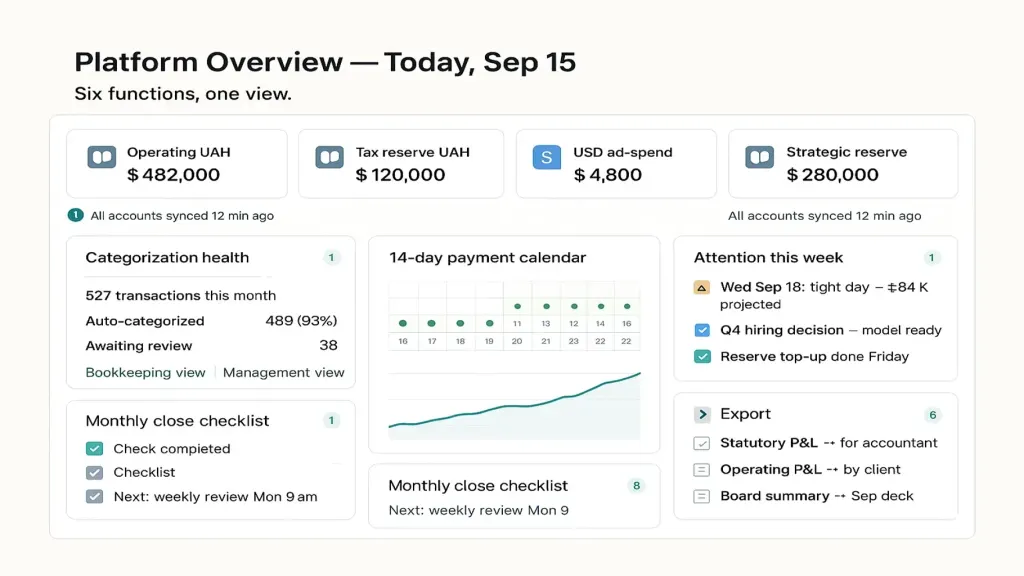

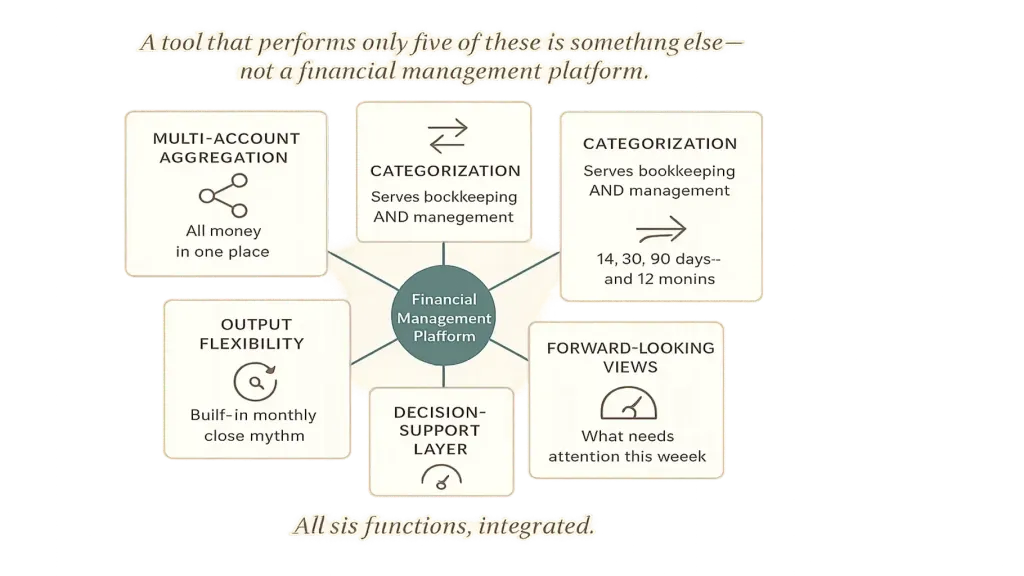

The Six Functions a Real Platform Performs

Stripping away the marketing language, a real financial management platform performs six functions. A tool missing any of these is something else — a bookkeeping app, a banking aggregator, a dashboard builder — but not a full management platform.

Function two — categorization that serves both bookkeeping and management. Every transaction tagged with enough detail to serve both the accountant (tax categories) and the owner (by client, by service line, by project). The tag structure rolls up cleanly into statutory categories and also slices into management categories without redundant work. The bookkeeping-vs-management distinction this addresses is the subject of article #2 → Bookkeeping vs Management Accounting →

Function three — forward-looking views. The 14- to 90-day payment calendar. The 12-month financial model. Scenario simulation for major decisions. A platform that only shows past data is just a bookkeeping report viewer — the forward views are what make it a management platform.

Function four — decision-support layer. A management dashboard summarizing the week's key signals (cash position, runway, AR aging, contribution margin trends, attention items). Alerts and exceptions, not just data dumps. A platform that produces 20 reports the owner has to sift through is failing — the platform should surface what needs attention.

Function five — workflow and cadence. Built-in rhythms for the monthly close, weekly review, quarterly strategic session. Reminders, checklists, automated report generation tied to actual calendar events. Without workflow, the platform becomes "yet another tab the owner doesn't open." Article #12 — Financial Control — covers the cadence side directly.

Function six — output flexibility. Statutory views for the accountant, management views for the owner, board-ready summaries for investors or advisors — produced from the same underlying transaction stream without manual re-entry. The platform multiplies one data input into many appropriate outputs.

A tool that does five of these well and misses one is incomplete. Most "accounting software" performs functions 1 and 2. Most "BI tools" perform function 4. Most spreadsheets attempt all six and degrade at three. A real financial management platform is built around the integration of all six.

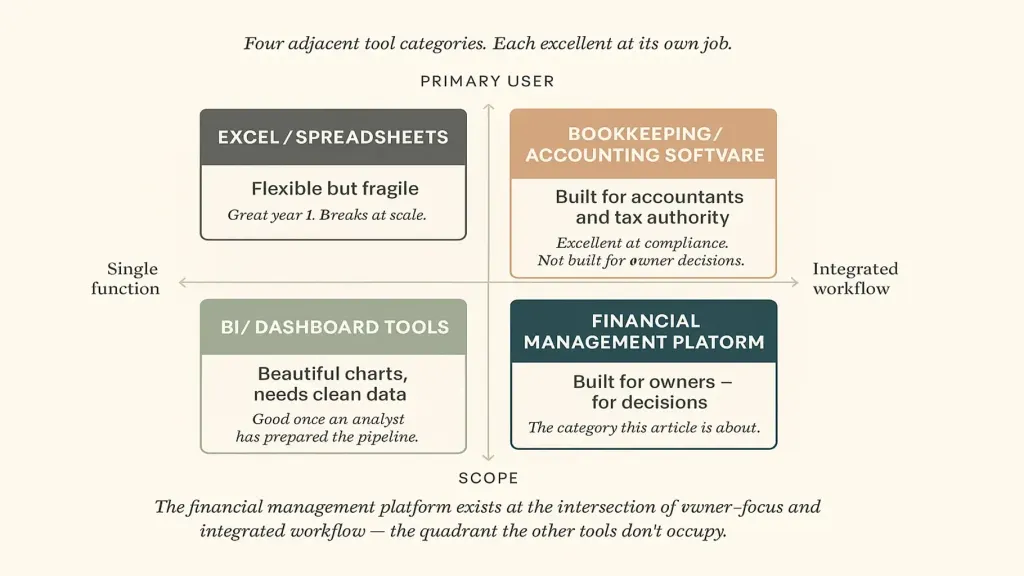

What It Isn't — Distinguishing From Adjacent Tools

The clearest way to understand a category is to draw its edges. A financial management platform is not:

Not a BI tool. BI tools (Power BI, Tableau, Looker) are general-purpose data visualization software. They can present financial data once it's been cleaned, modeled, and piped in. They cannot produce a payment calendar from a bank feed without significant setup work. They are platforms for analysts; financial management platforms are platforms for owners.

Not a spreadsheet. Spreadsheets are infinitely flexible and infinitely fragile. They serve as a perfect tool for the first 6–12 months of a small business's financial life. After that, the maintenance cost compounds: broken formulas, version drift, manual updates that get skipped, no audit trail. A financial management platform replaces the spreadsheet's structural functions while preserving the flexibility for the parts that need to remain custom.

Not a banking aggregator. Multi-bank aggregators (Plaid, Wise's multi-currency view) show you balances. They don't categorize. They don't forecast. They don't produce a P&L. They are the upstream data layer that a management platform builds on, not the platform itself.

Not a CRM-style "vibes dashboard." Some founder-facing tools produce attractive metric dashboards that are mostly directional ("revenue went up," "expenses went down"). Useful for marketing, insufficient for finance. A real financial management platform produces specific, decision-grade numbers (₴84K projected balance on Aug 27, client B contribution margin per hour of team time), not directional vibes.

The shape that emerges from these distinctions: a financial management platform sits at the intersection of bookkeeping, BI, and spreadsheet — and is specifically designed for the owner's decision-making.

Who It's For (and Who It's Not For)

Categories of business that benefit most from a financial management platform:

- Owner-operated businesses with revenue between ₴2 million and ₴30 million annually

- Multi-account or multi-currency setups (3+ accounts, FX exposure)

- Service businesses with project- or retainer-based revenue mix

- Businesses growing fast enough that mental tracking is no longer reliable

- Founders without dedicated CFO or finance director resources

- Businesses where the owner makes the strategic decisions (vs delegating fully)

Categories that don't yet need it:

- Pre-revenue or single-account businesses with one bank and one client

- Single-person solo operations under ₴1 million revenue with simple cash flow

- Enterprise businesses (₴100M+) that need full ERP

For the in-between cases — early-stage businesses considering when to adopt — the heuristic is simple: the moment you can no longer answer "how much cash do I have across all accounts?" in 30 seconds, you're past the point where spreadsheets are sustainable. That's the threshold where a platform becomes the right next step.

Build-vs-Buy Considerations

Some owners, especially technical founders, consider building their own platform — usually a custom dashboard on top of a database. This rarely works for the same reasons most custom-built internal tools fail:

- The build takes 6–12 months of attention that should go into the business

- Maintenance is permanent (bank feed APIs change, categories evolve, edge cases pile up)

- The first version solves the problems you knew about; the second and third versions are what actually deliver value, and those rarely get built

- An off-the-shelf platform built specifically for this purpose is now cheap enough that custom builds rarely make financial sense below ₴50M revenue

The honest answer for most businesses: buy the platform, configure it to your business, integrate it into your monthly close cadence. The implementation is days, not months.

📌 See what a financial management platform looks like in action — not in marketing screenshots, but in a working example of your kind of business. Book a 20-minute Finmap demo. We'll walk through the six functions on real example data and show how it would fit into your monthly close. Book a Finmap demo →

Read also

- How to choose financial management software

- Management accounting explained

- Accounting vs financial management

Topic foundation: Management Accounting Explained: What It Is and Why Owners Need It

Share valuable content — become a source of insights

Frequently Asked Questions

Does a financial management platform replace my bookkeeper?

No. The bookkeeper still handles compliance, monthly close mechanics, and tax-specific work. The platform makes their work flow into management outputs without manual re-entry, and produces views the bookkeeper doesn't usually generate (payment calendar, financial model, decision dashboard). The two work together. Article #2 — Bookkeeping vs Management Accounting → covers this division of labor.

Does a financial management platform replace my financial director?

No, and the inverse — a financial director without a platform is doing manual work that the platform would handle. The best setup combines both: the platform handles data aggregation, categorization, and report generation; the financial director (in-house or fractional) handles interpretation, strategic recommendations, and structural decisions. Article #8 — Outsourced Finance Director: When You Need One → covers this role specifically.

At what business size should I adopt a platform?

For most service businesses, the practical threshold is ₴2–3 million annual revenue OR 3+ accounts OR 5+ employees. Below those thresholds, a structured spreadsheet usually suffices. Above them, the spreadsheet's maintenance cost exceeds the platform's subscription cost within months. Article #9 — Financial Management for a Small Business → addresses the size threshold directly.

Can I just use a spreadsheet forever?

For a single-person business under ₴1 million revenue with one bank and a handful of clients — yes, with discipline. Past that scale, the spreadsheet stops being a tool and becomes a part-time job that distracts from the actual business. The owners who insist on spreadsheets after ₴3M revenue almost universally have a hidden cost — either a 5-hour-per-week maintenance burden or a reporting accuracy that quietly drifts.

How long does implementation take?

For a well-built platform: 1–3 weeks of configuration plus parallel running. The slow part is rarely the technology — it's getting bookkeeping clean enough that the platform's outputs are accurate. Article #1 — Management Accounting Explained → covers the foundation that needs to be in place.

What's the difference between this and a "CFO-as-a-service" subscription?

A CFO-as-a-service provides a person (an experienced finance professional working part-time for your business). A financial management platform provides software (the tooling that person — or you — uses). Many growing businesses use both: the CFO-as-a-service person works through the platform to deliver decisions and recommendations. Article #8 → discusses outsourced finance directors specifically.

Any questions left?

We are ready to answer them.

Finmap support