Table of Contents

939

11 min

12.06.2026

The Construction Firm With ₴18M in Signed Contracts That Couldn't Make Payroll

Sergiy Shuldik

Financial Expert at Finmap

"I had three contracts on the wall worth ₴18 million. And on Friday at 6 PM I was wondering how to pay for one truck of concrete."

The foreman called on a Friday evening, 6:14 PM. The concrete supplier had just confirmed: no payment by 8 AM Monday, no Monday pour. Twelve hundred cubic meters of foundation work — scheduled with the client for the following week, written into the contract, with a penalty clause for missed milestones.

No concrete on Monday meant no pour. No pour meant no progress invoice at the end of the week. No progress invoice meant no third installment from the client, which had been scheduled to clear "by mid-month."

The bank account that evening: ₴84,000. The Monday concrete invoice: ₴312,000. Wednesday's payroll for 14 people on the team: ₴487,000. The client's expected installment that the whole month depended on: ₴1,800,000.

The math had been done a dozen times since 5 PM. The owner had stopped opening the calculator app.

This is the story of a profitable construction company — ₴18 million in signed contracts on the wall, three active projects, two more in pipeline — that almost lost its team because of how cash flows in this industry. The crisis didn't end the company. But what changed afterwards is the part worth telling.

The Paradox: Profitable on Paper, Broken in the Bank

By every metric this business looked healthy. Three signed contracts totaling ₴18 million, all with reputable clients. A core team of 14 people who had been together for over two years. Margin on the residential complex alone — the largest of the three projects — was around 22%. On paper, the business should have been printing money.

The reality on Friday evening was different. Total liquid cash across all accounts: ₴84,000. Receivables that had cleared three different "expected" dates without arriving: ₴2.4 million. Subcontractor obligations due in the next 10 days: ₴890,000. Materials orders that had to be paid in advance to keep schedules: ₴540,000.

The owner had built the business by knowing construction inside out — every kind of foundation, every supplier, every subcontractor's quirks. What he had not built was a financial system that could see two weeks ahead. The Excel sheet on his laptop summarized last month's numbers, accurately and uselessly. It told him what had already happened. It said nothing about Monday.

"I knew every meter of rebar on every site. I couldn't tell you whether the company would survive next Wednesday." — site visit reflection, construction firm owner

Why Construction Is Structurally Fragile to Cash Gaps

Construction sits in an uncomfortable corner of the cash flow spectrum. Almost every structural feature of the industry pushes liquidity into a precarious position.

First: materials and subcontractors are paid upfront — clients pay in stages. The supplier wants payment before pouring concrete. The subcontractor wants 50% before mobilizing the crew. But the client pays after milestones are completed and verified — typically 30 to 45 days after the work is signed off. The bigger the project, the longer the gap between cash out and cash in.

Second: retention payments are locked away for months. Many construction contracts hold back 5–10% of every progress payment as retention — released only after final inspection. On a ₴10 million project, that's up to ₴1 million sitting in someone else's account for a year. Profitable, but not liquid.

Third: weather and inspection delays are exogenous. A two-day rain pushes the pour. The inspector reschedules. The client's procurement department is on holiday. None of these affect contract value — but every one of them affects when cash arrives.

Fourth: every project has its own cash rhythm. Three active projects mean three different milestone schedules, three different payment terms, three different sets of suppliers. Without a consolidated view, the owner is mentally juggling three calendars at once. Even a careful accountant can't hold all of it in working memory.

Fifth: scaling makes the problem worse, not better. A small contractor with one project at a time has a simple cash picture. A growing contractor with five active projects has five overlapping cycles — and if any two of them lag at the same time, the whole company is in a gap.

The owner's company was at exactly this scale. Three active projects. Two more starting in six weeks. Growing fast. And, as growth always does, devouring cash faster than it produced it.

5 Causes That Specifically Triggered the Crisis

Looking back at the next 30 days after the Friday call, five specific patterns emerged as the actual mechanism behind the cash gap.

Cause one. The largest client's payment was late — but not "late enough" to chase. The third installment on the residential project, ₴1.8 million, had been verbally promised for "mid-month." It came in 19 days late. Not catastrophic late. Not legal-action late. Just late enough that every plan downstream broke.

Cause two. Two subcontractor advances were paid in the same week. A roofing crew and a finishing crew both mobilized on the same Monday — both demanding 50% advance. Combined: ₴680,000 out the door in 48 hours. The schedule had been set months earlier; nobody had stress-tested whether the cash would be there.

Cause three. ₴1.2 million in retention payments across three projects. All locked away, all "earned" on paper, none available. On a healthy month this is invisible. In a tight month it is the difference between making payroll and not.

Cause four. A materials price increase nobody had budgeted for. Steel prices jumped 11% between contract signing and procurement. The contract was fixed-price. The supplier was not. The difference came out of working capital.

Cause five. The owner had been pulling personal income out of the business steadily. Not extravagantly — a normal monthly draw for a family with two kids. But timed against tight cash, those withdrawals were one more drain. He hadn't seen them as part of the cash problem because they "had always worked before."

Five causes. None individually catastrophic. All present in the same 30 days. Together — a Friday evening phone call about ₴312,000 in concrete.

What the Owner Did Monday Morning

The immediate weekend resolution was unromantic. A phone call to the largest client's finance director on Saturday morning ("we need ₴500,000 this week, the rest can wait two weeks"). An overdraft conversation with the bank Monday at 9 AM. A frank Sunday-evening conversation with the team's senior foreman, who agreed to delay his own salary by one week.

The concrete was paid. The pour happened on Tuesday instead of Monday. The client's penalty clause was avoided. The team did not lose anyone.

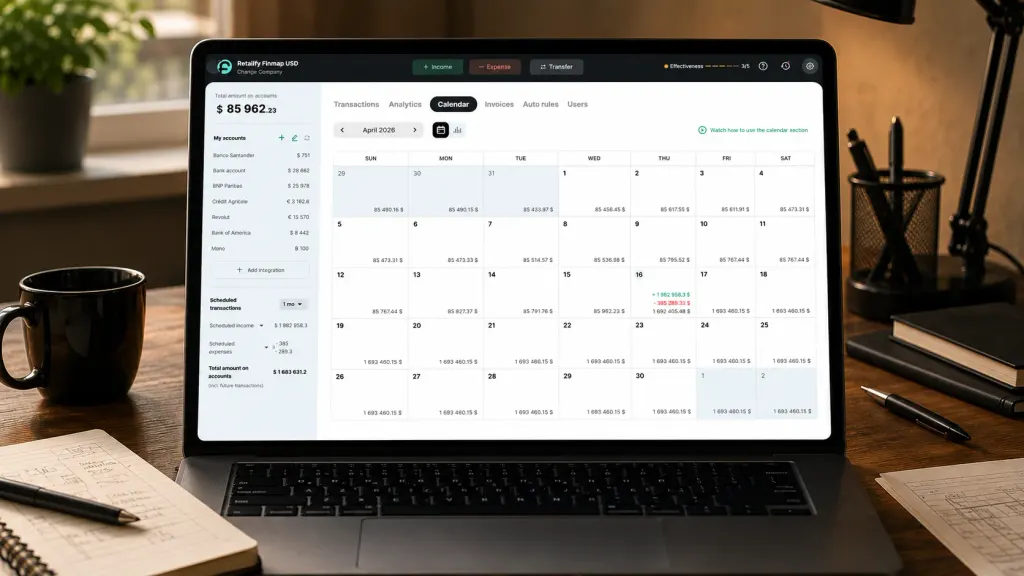

But the Monday after the dust settled, the owner did something else. He sat down with the accountant and they spent four hours building something the company had never had: a payment calendar that looked 14 days forward across all three projects simultaneously.

Not last month's summary. Not a P&L. A daily projected cash balance — today, tomorrow, the day after, every day for two weeks — built from every scheduled inflow (client milestones, retention releases when due, the bank line) and every scheduled outflow (subcontractor payments, materials orders, payroll, taxes, the owner's draw).

The first version was rough. Excel formulas, manual entry, three hours to update. But for the first time, the owner could see a number on Monday morning that told him whether Wednesday would be safe.

Within three weeks, the company had migrated from Excel to a proper financial planning tool. The calendar now updated automatically from bank feeds. It consolidated all three project cash flows into one view. It highlighted days where the projected balance would fall below the safety threshold — the owner had set ₴300,000 as the minimum.

The principle was simple. See the gap before it sees you.

90 Days Later — What Changed

Three months after the Friday call, the same business looked structurally different from the inside, even though the projects, the team, and the contracts were the same.

Average cash buffer. Before: ₴84K to ₴250K, fluctuating chaotically. After 90 days: ₴680K average, with a minimum of ₴340K. The buffer wasn't built by cutting costs. It was built by re-timing payments — pushing subcontractor advances by 5–7 days to match incoming client milestones, negotiating slightly better terms with two key suppliers, and stopping the owner's draw during the two highest-risk weeks of each month.

Visibility horizon. Before: 0 days — the owner discovered cash problems when bills arrived. After: 14 days standard, 30–45 days for major contracts. Decisions that used to be reactive ("can we afford this?") became proactive ("here's when we should schedule this").

Emergency overdraft usage. Before: 3 short-term overdrafts in 6 months, average cost 1.8% per drawdown. After 90 days: zero. The overdraft line still exists as a safety net — but it has not been touched.

Payroll surprises. Before: 2 instances in the previous year of "we'll pay on Friday instead of Wednesday" conversations. After: zero. Wages clear the same date every month, no exceptions.

Client communication tone. Before: defensive, often delayed responses when clients asked about schedule. After: the owner now opens conversations about retention release timing and milestone scheduling proactively — because he knows what's coming and when he needs it.

The hidden change is harder to measure. The owner used to spend roughly two evenings a week thinking about cash — running mental simulations of which payment could be delayed, which client to chase, what to do if X didn't come through. After the calendar was in place, those evenings vanished. The same questions still existed — but they had answers ready in advance.

The Owner's Reflection

"I used to think a financial system was something you build when you've outgrown the size where you can hold it all in your head. Wrong. You build it the moment you have more than one project running at once. By the time you can't hold it in your head, you've already missed two payrolls."

The owner now describes the change in two parts.

The visible part: a payment calendar that consolidates three projects, updates from banks automatically, and shows him 14 days forward every Monday morning. He spends 20 minutes with it each week.

The invisible part: a complete shift in how decisions get made. Quotes for new projects now include a cash flow simulation before the price is sent. Subcontractor schedules are tested against the calendar before crews are mobilized. Retention release dates are tracked individually and chased two weeks before they're due. Personal income from the business is timed against high-cash weeks, not "whenever."

The company is currently working on its fifth project simultaneously. The calendar still works. Headcount is now 19. Margin has improved by 3 percentage points across the active portfolio — not because the work changed, but because the rare emergency-mode decisions (pay this subcontractor faster than necessary, accept worse terms from a supplier under time pressure) have stopped happening.

The Friday call that started this story did not recur.

Topic foundation: Cash Flow Gap: How to Identify It and How to Prevent It

Industry: How Finmap Helps Construction Businesses Regain Financial Control

Share valuable content — become a source of insights

Frequently Asked Questions

Does a payment calendar help if I run only one construction project at a time?

Yes, but the gain is smaller. With one project, you can often keep the cash picture in your head. The real value of the calendar shows up the moment you have two or more projects with overlapping milestones — that's when the mental model breaks down and most cash gaps happen.

What's a reasonable cash buffer to keep for a construction company?

Two to three months of fixed costs (wages, office, recurring overhead) plus a reserve for materials advances on the largest active project. For a company with ₴500K monthly fixed costs and ₴800K typical materials advance, that's roughly ₴1.8–2.3 million. Most contractors run below this level — and almost all of them experience cash gaps as a result.

How long does it take to set up a payment calendar?

First working version: 2–4 hours, even with manual entry. Bank-feed integration and automatic updates: another 4–6 hours over the first two weeks. After that the system maintains itself with 15–30 minutes of attention per week.

Can I do this in Excel instead of a dedicated tool?

For one or two projects — yes. For three or more, Excel becomes a part-time job. The maintenance cost grows faster than the value. The most common failure mode is that the Excel file becomes a week behind reality, which makes it worse than no calendar at all (because you trust it and it lies).

What about retention payments — how should I plan for those?

Track every retention amount separately by contract and by expected release date. Treat them as receivables with a known maturity, not as available cash. Then plan two cash buffers: one for operations, one specifically sized to absorb the gap between when retention is "earned" and when it actually arrives.

Is this only for medium-sized construction firms?

No. The smaller the contractor, the less margin for error. A 3-person crew with one ₴2 million project has the same structural cash gap as a 30-person firm — just with smaller absolute numbers. The calendar is more, not less, important at small scale.

Any questions left?

We are ready to answer them.

Finmap support