Table of Contents

262

5 min

25.06.2026

Cash Flow Gap: How to Identify It and How to Prevent It

Oleksandr Solovei

CEO & Co-founder Finmap

"We were profitable in October. We were profitable in November. And on November 14th, I couldn't pay the salaries. That's when I learned that profit and cash are not the same thing — they live on different calendars."

A founder of an ₴8M product business described the night before payroll, two years ago, that taught her what a cash flow gap actually is.

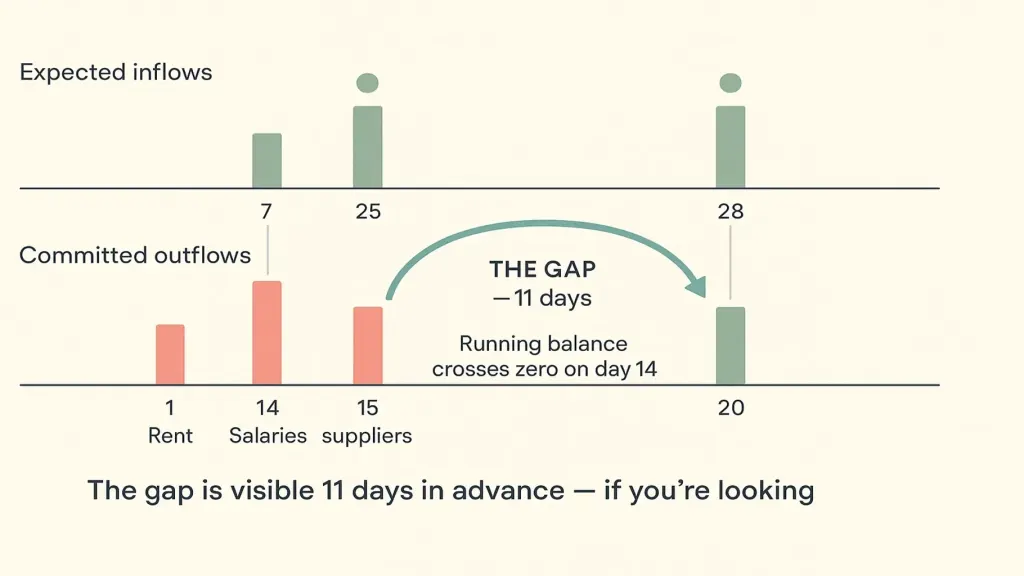

October had been a strong month. November was on track to be stronger. Her management P&L showed both months solidly profitable. And on November 13th — the day before salaries had to go out — she logged into her bank account and saw a balance that wouldn't cover them.

Nothing had gone wrong operationally. Sales were strong. Margins were healthy. The business was healthy. And she couldn't pay her people on Friday, because the money that would make her profitable in November wasn't going to arrive until November 25th — and salaries were due on the 14th.

That gap between when money is earned and when money arrives is what every small business owner eventually learns is the single most important pattern in operational finance. Not whether the business is profitable. Whether the cash is in the account on the day it's needed.

This article is about identifying that gap before it bites, and the four practices that prevent it from happening twice.

The Definition That Matters

A cash flow gap is the period of time between a committed outflow and the inflow that was supposed to fund it. It's not the same as a cash flow problem (chronically more outflows than inflows). It's a timing problem inside an otherwise healthy business.

A profitable business with a cash flow gap is in worse danger than an unprofitable business without one — because the profitability hides the urgency. The owner is making money on paper, which makes it psychologically harder to take the operational steps that prevent the gap from happening again.

In small business specifically, the gap shows up most commonly in three patterns:

- The end-of-month convergence: salaries on the 15th, rent on the 1st, tax on the 20th — all clustered, and inflows that come irregularly through the month.

- The growth-funded-gap: business is growing fast, so working capital (inventory, prepaid suppliers, salaries for new hires) goes out before the revenue from those investments comes back.

- The seasonal mismatch: a few strong months a year, but expenses spread evenly across all twelve.

The general framework — what management accounting actually means, and why this is one of its central problems — is in the anchor article → Management Accounting Explained.

How to Identify a Cash Flow Gap (Before It Hits)

The single most useful tool for spotting a cash flow gap is the 30-day payment calendar. Not the bank balance — the bank balance tells you about today. The payment calendar tells you about the day in two weeks when nothing changes operationally but the balance won't be enough.

Confidence and criticality are the parts most owners skip. Listing inflows without confidence levels means the calendar will be optimistic — every owner believes every client will pay on time, and most won't. Listing outflows without criticality means there's no priority order when the gap appears — every payment looks equally mandatory, when in reality some can be moved by a week with a phone call.

A good payment calendar shows you the gap two weeks in advance. A bank balance shows it to you the morning of. Two weeks is the difference between "I'll call the client and ask if they can pay early" and "I need to take out a personal loan tonight."

The full how-to is in the payment calendar article → Payment Calendar: Why and How.

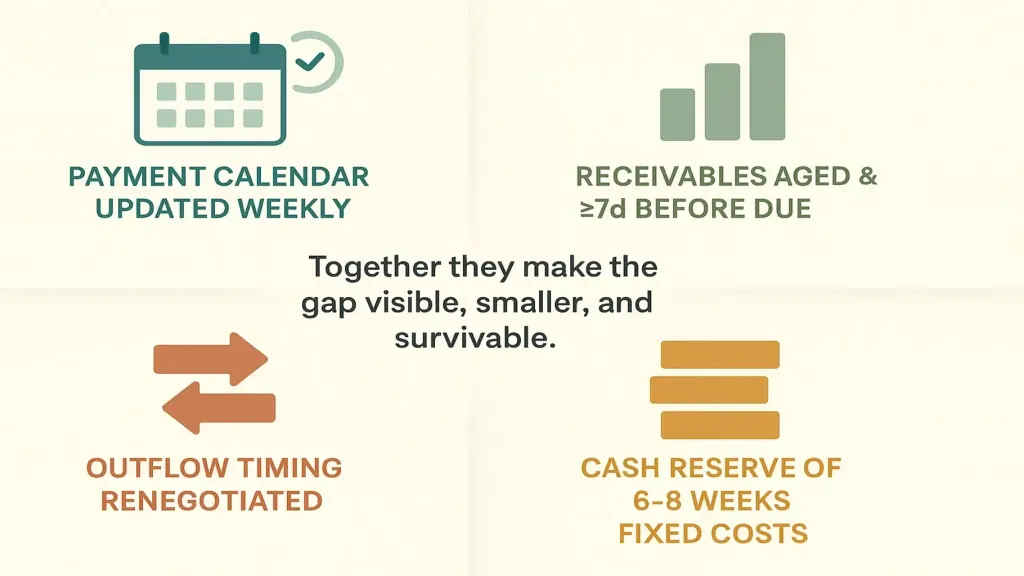

The Four Practices That Prevent Cash Flow Gaps

Two — age and chase receivables before they're late. Most clients don't pay late maliciously. They pay late because the invoice is below their attention threshold. A polite reminder seven days before due date, then on the due date, then three days after, recovers most of what would otherwise be quietly late. The owners who do this well report 60–70% improvement in average days-to-pay.

Three — renegotiate outflow timing where possible. Most suppliers, landlords, and even tax-installment programs have more flexibility than owners assume. A request to move the rent from the 1st to the 5th — once, in writing — often gets approved because the landlord wants the rent more than they want the date. The same is true for many supplier invoices. The owner who never asks pays on the day everyone else does.

Four — keep a cash reserve of six to eight weeks of fixed costs. This is the structural backstop. Not for the predictable gaps — those should be solved by the first three practices. The reserve is for the unpredictable gap: a client who suddenly stops paying, a supplier price spike, a slow month nobody saw coming. Six to eight weeks of fixed costs only (not total expenses) is the standard small business target. More if seasonality is severe, less if revenue is highly predictable.

These four together don't eliminate cash flow gaps — they make them visible early, smaller in size, and survivable when they arrive.

What to Do When the Gap Is This Week

Sometimes the discovery happens too late. A 14-day gap with seven days to solve it. Here's the operational sequence.

Day 1–2 — pull forward what you can. Call the two biggest expected receivables. Offer a 1–2% early payment discount for a payment in three days. Send fresh invoices to anything that's been delayed. Charge any sales that are awaiting your invoice.

Day 2–3 — delay what you can. Call the biggest non-critical outflows. Ask the supplier to move payment by a week. Most will, especially if asked once and never twice. Move any payments that are about to auto-debit but aren't time-critical.

Day 3–4 — make up the rest from reserves. This is what the reserve is for. Tap it. Don't tap personal credit unless reserves are exhausted.

Day 5 onward — install the practices that prevent it next time. The most expensive part of a cash flow gap is the second one, three months later, when you haven't installed the system that would have flagged it.

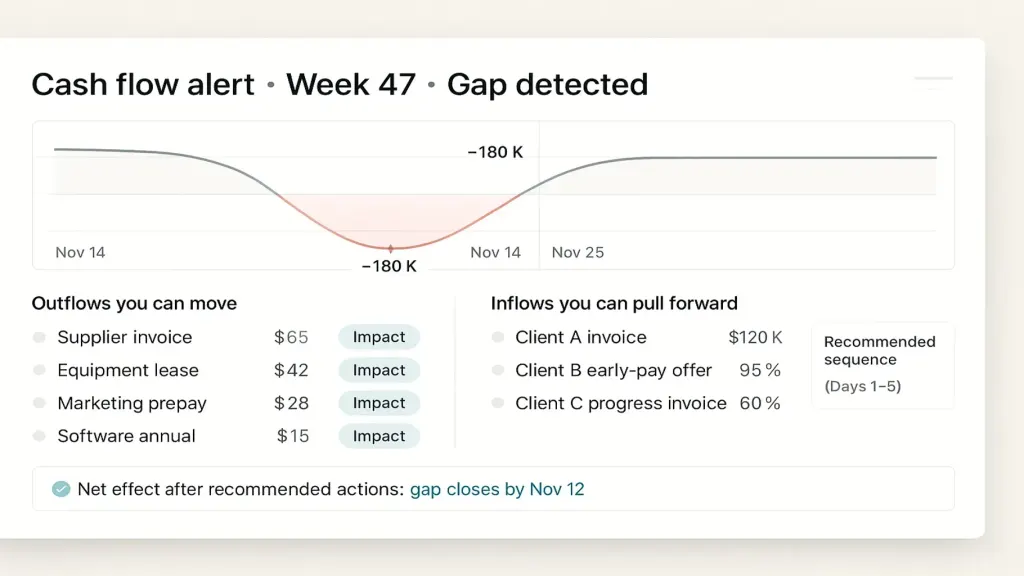

📌 See how cash flow gaps become visible weeks in advance — payment calendar, receivable aging, reserve tracking — in one integrated view. Book a 20-minute Finmap demo. Book a Finmap demo →

Read also

- How to avoid cash gaps in your business

- How to build a payment calendar to close a cash flow gap

- Finmap Findirector: control your cash flow

In this topic

- 8 Financial Lessons After Losing $120,000: How to Avoid Cash Gaps

- 5 Tips to Eliminate Cash Flow Gaps Permanently

- What Is a Cash Gap and How to Stop It

- The Friday Question: Which Supplier Gets Paid This Week?

- ₴500K in May, ₴160K in July: The Cashflow Discipline Seasonal Businesses Skip

- From Seasonal Slumps to Steady Profit: How to Earn All Year Round

- The Construction Firm With ₴18M in Signed Contracts That Couldn't Make Payroll

Topic foundation: Cash Flow Management for a Small Business: How to Always Know Where Your Money Is

Share valuable content — become a source of insights

Frequently Asked Questions

My business is profitable. Why do I still have cash flow gaps?

Profitability is a period concept (the month, the year). Cash is a moment concept (Tuesday at 9am). They're tracked on different calendars. Profitable businesses have gaps when the period and the moment don't align.

Is a credit line a substitute for the four practices?

A credit line is a backstop, like the reserve. It's not a substitute for the calendar and the discipline. Owners who rely on the credit line without the calendar tend to draw it down structurally and find themselves in a worse position 12 months later.

How big should my cash reserve be?

Six to eight weeks of fixed costs only (salaries, rent, recurring subscriptions, tax obligations). Not total expenses, which would be too high for most small businesses to maintain. Adjust upward if seasonality is severe.

Should I solve this with a spreadsheet or a platform?

Spreadsheet works for the first 6–12 months and most micro-businesses. A platform makes sense when maintenance becomes painful — typically once you have 3+ accounts, multiple currencies, or 30+ recurring outflows.

What if I can't even get to six weeks of reserve?

Start at two weeks. Build it from gross margin on every sale until you reach six. The reserve takes 18–24 months for most small businesses to build from zero. Start now.

Is this the same as a cash crisis?

No. A cash crisis is structural (outflows chronically exceed inflows). A cash flow gap is a timing mismatch in an otherwise healthy business. The interventions for each are completely different.

Any questions left?

We are ready to answer them.

Finmap support