Table of Contents

629

11 min

18.06.2026

The Friday Question: Which Supplier Gets Paid This Week?

Sergiy Shuldik

Financial Expert at Finmap

"On Friday morning I had three suppliers expecting payment, ₴180,000 in the operating account, and ₴210,000 total owed by Tuesday. I had to choose which one to delay. The thing is — our revenue that month was the best in two years."

She runs a digital marketing agency. Six years old. Eight people. Annual revenue: ₴3,600,000. The previous month had closed at ₴340,000 — the best month she'd had since launch. By every metric of "is the business healthy," the answer was clearly yes.

And on Friday morning, sitting with her coffee, she had to make a small humiliating decision: which of three suppliers to delay.

Her largest client — ₴65,000 retainer — had paid Wednesday as agreed. Two project clients were due to pay "by end of next week" — meaning anywhere from Tuesday to Friday. A printing supplier wanted ₴48,000 by Monday. A subcontracted designer wanted ₴62,000 by Tuesday. The freelance copywriter who'd just finished a launch needed ₴35,000 by Friday. Plus ₴42,000 in salaries on Wednesday.

She had the money. Just not on the days she needed it.

That Friday morning was the catalyst for the most boring, most useful financial tool a small business owner ever installs: a payment calendar. This article is about why it's necessary even when revenue is fine, what makes a real one work, and how to build one over a weekend.

The Paradox: Revenue Fine, Cash Painful

Most founders, when they think about "cash flow problems," picture a business that's losing money. The picture is wrong. Most cash flow problems are timing problems in profitable businesses.

The numbers don't lie about whether the business is profitable. The agency's monthly P&L showed a healthy 24% operating margin. Year-to-date, she was up 19% vs. the prior year. Three new clients had signed in the last two months. There was nothing wrong with the business.

What was wrong was the temporal relationship between cash in and cash out. Clients paid on their own schedules — some on the 5th, some on the 15th, some "by end of month," some when they remembered. Suppliers expected payment on their schedules — many of them on the 1st or 15th, indifferent to when clients had paid. Salaries were due on fixed dates. Taxes had their own quarterly rhythm. None of these calendars coordinated with each other.

The bank account is the place where all these mismatched calendars collide. When you look at your bank balance, you're looking at the random intersection of a dozen overlapping cash schedules. Sometimes the intersection looks healthy. Sometimes it looks alarming. Almost never does the bank balance tell you anything about the next 14 days, which is when the actual decisions need to be made.

"I didn't have a money problem. I had a timing problem. Until I'd built a payment calendar, I couldn't tell those two apart — and I made decisions as if both were the same."

What a Payment Calendar Actually Is (and Isn't)

A payment calendar is not a budget. It's not a P&L. It's not a forecast of profit. It's not a cash flow statement in the accounting sense.

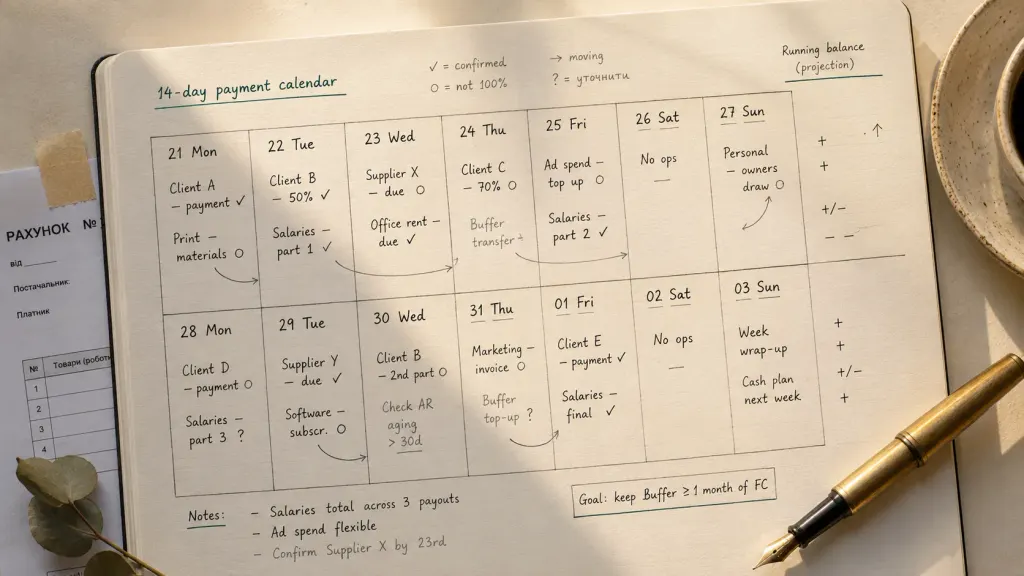

A payment calendar is a single document — paper, spreadsheet, or tool — that shows, for each of the next 14 to 90 days:

- Every scheduled inflow (client payments, retainers, refunds, expected proceeds)

- Every scheduled outflow (supplier payments, salaries, taxes, subscriptions, owner draws)

- The projected balance on each day, calculated as: previous day's balance + inflows − outflows

That's it. The simplest version is a single table with three columns. Date, in/out, projected balance. The most sophisticated version is a multi-account dashboard with automated bank integration. The discipline is the same.

What it gives you that nothing else does:

- Knowledge of which exact days will be tight, 14+ days in advance

- The ability to renegotiate timing rather than amount (much easier to win)

- The end of the Friday-morning question about which supplier to delay

- A defensible basis for telling a client "we need payment by date X to keep your project on track"

- The freedom to take strategic actions (early-pay discounts, supplier negotiations) instead of reactive ones

What it isn't:

- A solution to actual unprofitability (if you're losing money, the calendar reveals it but doesn't fix it)

- A substitute for the monthly P&L review or quarterly strategic review

- A replacement for honest pricing or for client receivables management

- A guarantee against surprises (a major client folding still hits hard — but you see it sooner)

The payment calendar is a timing tool. That's its entire job.

The Four Building Blocks of a Real Payment Calendar

A working payment calendar has four building blocks. Skip any one of them and the calendar gradually loses contact with reality and gets abandoned within a quarter.

Block one — the account map. A complete inventory of every place where the business holds money. Operating UAH. Tax reserve. Strategic reserve. USD account. EUR account. Petty cash. Payment processor float. Client prepayments held in a separate sub-account. A surprising number of payment calendars fail because they were built on "the main account" — and the main account isn't where all the money is. The account map is the foundation of the calendar's accuracy.

Block two — the inflow ledger. Every expected payment from a client, lender, or other source. For each entry: which client, how much, expected date (best-guess, not promise), confidence level (high/medium/low). The confidence level is what separates a wishful-thinking calendar from a useful one. A ₴65K retainer from a four-year client on the 5th of the month is high-confidence. A project final payment from a new client "expected by end of next week" is medium. A late wholesale invoice from a chronic late payer "should arrive this week" is low.

Block three — the outflow ledger. Every committed payment from the business. Recurring (salaries, rent, subscriptions, tax payments on known dates). Variable (supplier invoices that arrived this week, expected materials orders, freelance contractor invoices). Each entry: payee, amount, due date, criticality (must-pay on date / flexible by a week / negotiable). The criticality column is what lets you renegotiate timing instead of amount when a pinch appears.

Block four — the daily projection. A simple running balance calculation across all accounts: starting balance + inflows − outflows = ending balance for the day. Extended forward 14 to 90 days. The projection is where the calendar earns its keep — by surfacing the days that will be tight, the days that will be surplus, and the gaps between income and outgoing that can't be solved by waiting.

These four blocks, working together, are what convert "I look at my bank account three times a day and feel anxious" into "I know what every day of the next two weeks looks like, including which days have slack and which need attention."

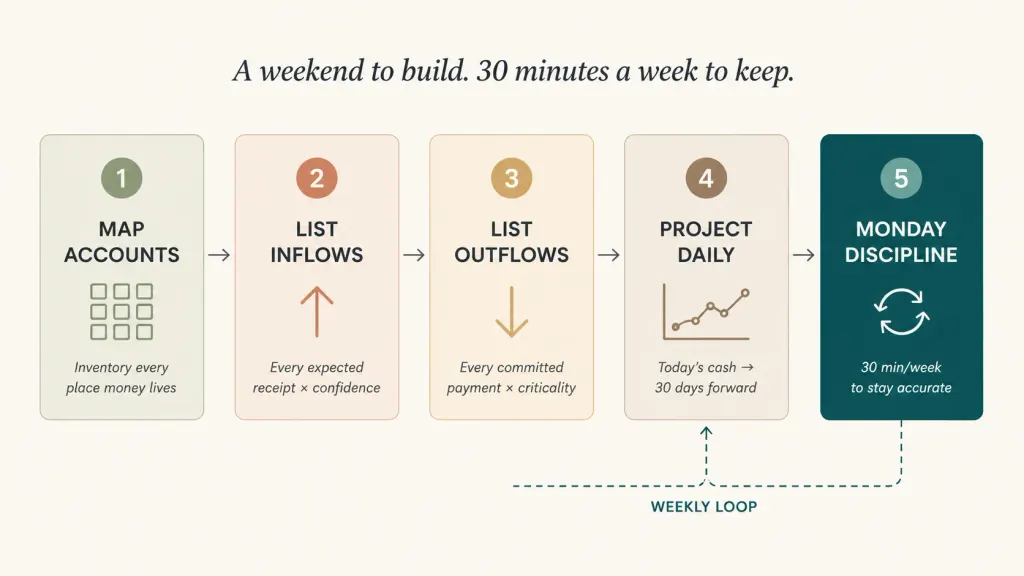

How to Build One Over a Weekend — The 5-Step Process

The first version takes about 4 hours of focused time. Most founders break it across a Saturday and Sunday.

Step one — map every account, every wallet, every cash location. List them all. For each: today's balance, currency, the typical activity it sees. For the agency, this turned out to be: Operating UAH, Tax UAH, Strategic UAH (newly created), USD ad-spend account, payment processor float, petty cash at the office. Six locations totaling more than she had thought.

Step two — list every expected inflow for the next 30 days. Go through every active client. For each: when do they typically pay, how much, how confident. Then add: every outstanding invoice that hasn't been paid yet (with confidence based on the client's track record). Add any other expected income — refunds, returns, advisor payments, the EU grant you applied for. Mark each with high/medium/low confidence.

Step three — list every expected outflow for the next 30 days. Recurring first: salaries (with their exact dates), rent, every subscription you can think of (you'll discover 30% more than you remembered), tax payments on their known dates, the accountant. Variable second: every supplier invoice currently in the inbox, every expected material order, every freelance payment due. Mark each with criticality: must-pay date / flexible by a week / fully negotiable.

Step four — project the daily balance forward. Start with today's total cash across all accounts. For each day, add expected inflows and subtract expected outflows. The result is a column of ending balances per day for the next 30 days. The first time you do this, expect surprises. Most founders discover at least one tight day in the next 14 they hadn't been aware of, and at least one surplus day that gives them strategic options they hadn't seen.

Step five — install the Monday discipline. Every Monday morning, 30 minutes: update the calendar with what actually happened last week (which payments came in, which didn't, which surprises hit), and extend the projection by another week (so it's always 30 days forward). This is what keeps the calendar alive. Without the Monday discipline, the calendar is accurate for 7 days and then increasingly fictional. With it, the calendar is the most reliable financial document in the business.

The first build is the heaviest. The Monday discipline is much lighter — once the structure exists, updating it takes 25–35 minutes.

What a Payment Calendar Enables — And Doesn't

Having the calendar in place changes the type of decisions you can make.

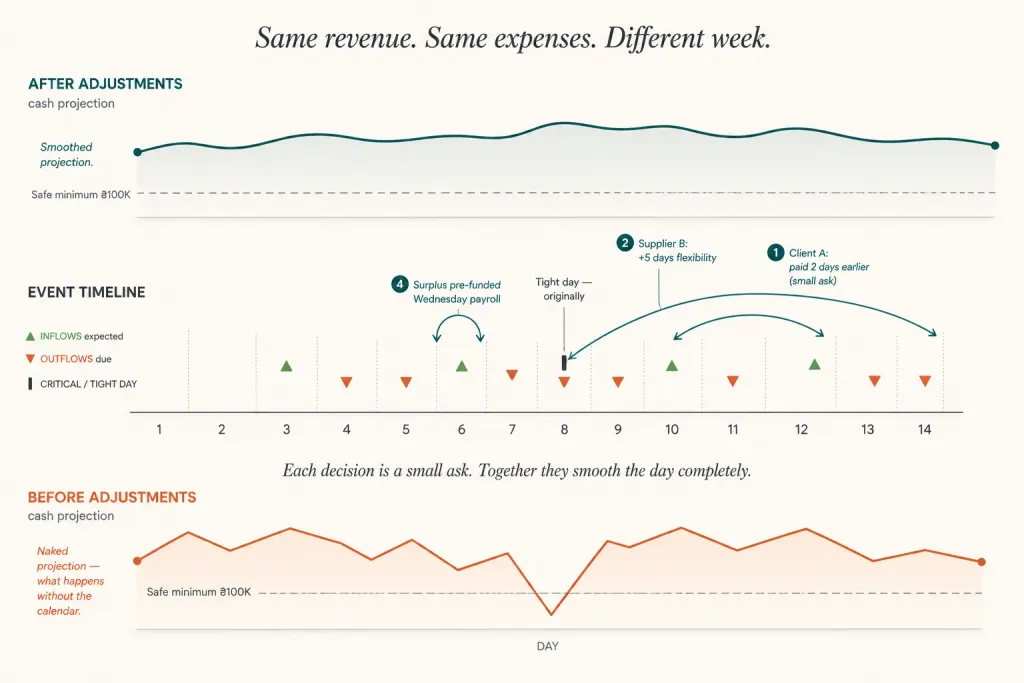

It enables timing negotiations instead of amount negotiations. When a tight day shows up 12 days ahead, you have options. You can call the largest client whose payment is due that week and politely ask if it could clear two days earlier. You can call the supplier whose invoice has flexibility and ask for an extra 5 days. You can offer a small early-pay discount to a wholesale buyer. You can postpone a non-critical equipment order by a week. Each of these is a small ask. Done together, they smooth the day completely.

It enables real conversations with clients about payment terms. Instead of being defensive when a client asks about pricing, you can have a structured conversation: "Our net-30 terms only work if you actually pay net-30. The 3 of the last 6 invoices have been net-45 to net-50. Can we agree on net-30 with a structured reminder, or shift to net-45 with appropriate pricing?" This is a different conversation than vague stress about late-paying clients.

It enables strategic use of surplus days. When the calendar shows a surplus week, you can use it deliberately: top up the strategic reserve, prepay a supplier for a discount, settle the freelance invoice that's been hanging around, take the owner draw you've been postponing. Surplus weeks that pass unused are wasted optionality.

It doesn't fix structural problems. If clients consistently pay 30 days late on a 30-day term, the calendar shows it but doesn't fix it — you fix it by renegotiating contracts or moving clients. If margins are too thin, the calendar shows that you're always tight by the 25th, but doesn't change the underlying margin. If a key client represents 40% of revenue, the calendar can't make that risk disappear. The calendar reveals truth — it doesn't transform it.

What Changed for the Agency in 90 Days

Three months after the Friday-morning supplier dilemma, the same business looked structurally different.

The Friday question stopped happening. By the third weekend with the calendar in place, the founder could see Friday morning's likely cash position by the previous Monday. Pinches were renegotiated before they became urgent — usually by Tuesday or Wednesday of the prior week. Suppliers stopped getting asked to wait, because they were paid when they expected to be paid. One supplier mentioned this in passing and offered a 1.5% discount for consistent on-time payment.

Client payment terms cleaned up. The calendar made visible which three clients were chronically 15–25 days late. The founder had structured conversations with each: one upgraded to a deposit + balance arrangement, one moved to direct debit on the 5th, one accepted a 3% surcharge for net-45 terms. Aggregate days-late across the receivables book dropped from 18 to 4 over 60 days.

Strategic reserve became fundable. The calendar showed that two specific weeks each month had reliable surplus. Automatic transfers were set up on those weeks — ₴18K total per month into the strategic reserve. After 12 weeks, the reserve had grown from ₴0 to ₴54K. By the same time next year, it should be over ₴200K — enough to absorb a major client loss.

Founder anxiety dropped sharply. Before the calendar, the founder checked the operating account 6–8 times a day. After, the Monday morning 30-minute review was the only time she looked. The bank app went into a folder she didn't open. The mental space freed up went into client work and a planned launch of a new service line — which delivered ₴280K in incremental revenue in Q4.

"The calendar didn't change how much I earned. It changed what I could do with what I earned. That's a different kind of business."

Read also

Topic foundation: Cash Flow Gap: How to Identify It and How to Prevent It

Share valuable content — become a source of insights

Frequently Asked Questions

Do I really need this if my business is small?

If you have one supplier and one client, you probably don't. From the moment you have 3+ recurring outflows, 2+ clients with different payment schedules, or any meaningful variable costs, the calendar starts paying for itself. By the time you're a 3-person business, it's essential.

Spreadsheet or specialized tool?

For the first month, spreadsheet is fine — it forces you to understand the math. After 30–60 days of manual updates, most owners switch to a tool because the Monday discipline gets harder when reality moves faster than the spreadsheet. The right answer depends on how complex your account map is. With 2–3 accounts, spreadsheet works indefinitely. With 5+ accounts and bank integrations, a tool with auto-update is what makes the Monday discipline sustainable.

How far ahead should the calendar project?

14 days is the minimum useful horizon. 30 days is the sweet spot for most service businesses. 60–90 days makes sense if you have seasonality, long client billing cycles, or large planned commitments. Don't try to project 180 days unless you have a specific reason — the further out you go, the lower the confidence and the higher the maintenance cost.

What if my clients' payment dates are unpredictable?

That's exactly when the calendar is most valuable. The point isn't to have perfect predictions — the point is to make the unpredictability visible. A column for "high/medium/low confidence" on each inflow surfaces which clients you can plan around and which you can't. The unreliable payers become specifically identified rather than vaguely worrying.

Should taxes and owner draws be in the calendar?

Yes, both. Taxes go in as scheduled outflows on their known dates. Owner draws go in as scheduled outflows on the dates you've decided (see our owner dividends framework). Many calendars fail because the founder mentally treats their own pay and the business's taxes as "different" — they're not, from the calendar's perspective. Every outflow counts.

What about multi-currency businesses?

Add a column for currency on each line. Use today's rate for the projection (don't try to forecast FX — that's a different problem). The projection shows balances per currency; you can convert to a common currency for the bottom-line summary if useful. Most multi-currency businesses overcomplicate this — keep it simple.

Any questions left?

We are ready to answer them.

Finmap support