Table of Contents

"But we're profitable. So why is there no money in the account? How is that even possible?"

A familiar scene. It's the 12th of the month. Rent is due tomorrow — UAH 18,000. Payroll is the day after — UAH 92,000. Your current account holds UAH 31,000. A big client promised to pay "by Friday" — and today is Wednesday.

You open your phone again and check the statement. Still the same number — UAH 31,000. The math starts spinning in your head: "If I push rent back 3 days… well, the landlord already reminded me last time. If I call the client today, that's the fourth call this week. If I take a short overdraft, that's -2.5% per week. If I just delay payroll, then tomorrow one of the salespeople quits, telling me straight 'I don't expect anything more from this.'"

You'll remember this evening for a long time. This is a cash gap.

And the worst part of the story is that you could have seen this gap coming 14 days earlier. Not on a Wednesday evening in a five-day panic, but calmly, back last week. In this article we'll break down what a cash gap is, why it happens even to profitable businesses, and what to do this very week so you can spot the next gap in advance.

What a cash gap is — without the accounting jargon

A cash gap is the moment when there's no money in your till or account, even though the business is profitable overall.

Put more simply: picture a water pipe. Money flows into the business (clients pay) and out of it (suppliers, payroll, rent). If the inflow suddenly slows down — say, a client drags out a payment — while the outflow stays the same (rent doesn't wait), an empty stretch forms in the pipe. That's the gap.

It's not about profit. It's about timing. A business can earn millions a year, but if you paid a supplier on Monday and the client's money won't arrive until the following Monday, then on Tuesday you may simply not have enough to cover an urgent expense.

The paradox: why cash gaps often hit profitable businesses

Intuitively it seems that if a business is growing, money should be fine. The reality is the opposite.

The faster you grow, the greater the risk of a cash gap. It's not a bug, it's a feature of growth.

There are three reasons. First — more clients means more receivables. You have more issued invoices that haven't been paid yet. Second — more obligations. A bigger team means bigger payroll every month. More orders means more prepayments to suppliers. Third — the inertia of decisions. You signed a contract three months ago based on the balances you had at the time. Today your cash flow schedule looks different.

A classic situation — in December the business signs a long contract with a big client. It hires a large team in February. In March it also stocks up on raw materials in advance. And the first payment from the new client won't arrive until May — a 45-day payment deferral. Between March and May, that's two months of cash gap. On paper, a successful contract. In reality, two months without payroll or living on a credit line.

"There's a liquidity mismatch in payments — amounts may not arrive in the last days of the month, they come in at the start. And the supplier is waiting until the 20th." — a typical way a service-business owner puts it

5 typical causes of a cash gap

In consultations with small and medium business owners, we singled out the five most common scenarios. You may recognize one of them.

First. The gap between the deposit and the second payment. This happens in any business where the client pays in installments. Translation agencies, legal services, event agencies, construction. The client pays 50% at the start, the business does the work, pays suppliers/subcontractors in advance — and the client's second payment "gets stuck" for weeks or months.

Second. Overdue receivables from large clients. A corporate client has a 30-day payment deferral. That's normal in the market. But if the client pushes payment back a week — while rent has to be paid on the 1st of every month — you're already in a gap. It hurts especially when a single large client accounts for 40% of turnover.

Third. Seasonality. Clearest in retail: December carries February's revenue. But payroll, rent and bookkeeping fees are the same every month. A cash gap in February is a structural inevitability if you don't anticipate it back in November.

Fourth. Growth that outpaces cash. That same new big contract. You hired people. You bought raw materials. The first payment comes in 45 days. And payroll is due today.

Fifth. The owner's personal spending. Less pleasant, but real. The owner starts pulling money out of the business for personal goals (a house, a car, a vacation) at a time when current cash doesn't yet allow it. This also creates a gap — only its source isn't the clients, it's the owner.

What all five have in common is that the owner finds out about the gap too late. Often at the moment a payment is due and there's no money. Sometimes from a stressful call from a supplier. In the worst cases, from an alarming bank notification: "Your account has insufficient funds."

The first step to solving it — seeing your gap 14 days out

A cash gap can't be eliminated entirely by magic. But it can be predicted 14 days out — and that fundamentally changes the decisions you make today.

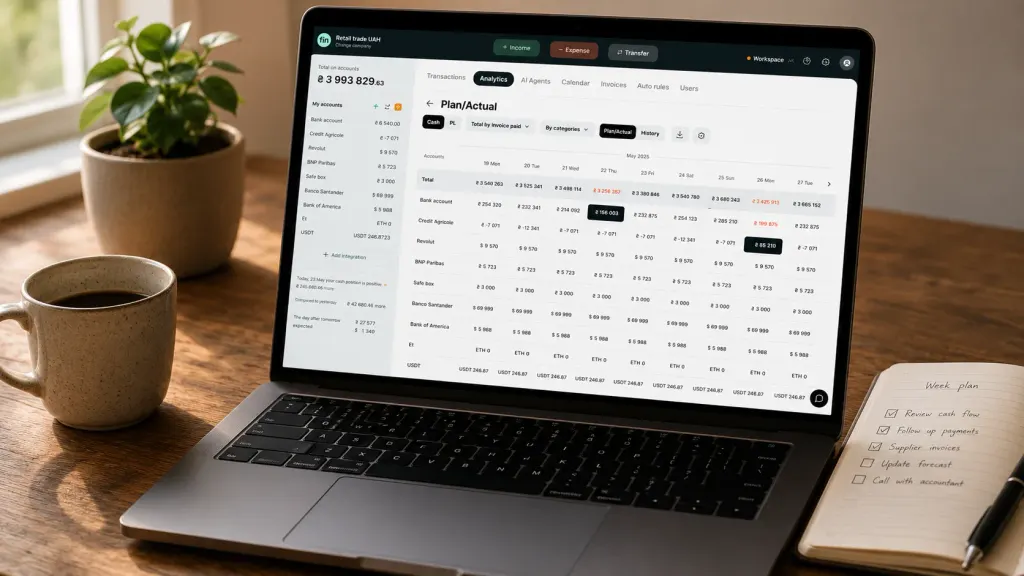

The tool that does this is the payment calendar. It takes all planned inflows (issued client invoices, expected deposits, recurring contracts) and planned outflows (rent, payroll, recurring subscriptions, direct supplier payments), and assembles them into a simple day-by-day forecast of your account balance.

Here's what a payment calendar gives you that an Excel sheet with monthly totals can't:

- You see day-by-day detail — exactly which day will be "red"

- It highlights the risk automatically — the day the balance drops below a safe threshold

- It updates itself from bank integrations — without daily manual edits

- It works on a 30–90 day horizon — which is critical for seasonal businesses

The key mechanic is just one: you see your future cash gap before it happens. Not on the evening of the 15th in a panic. But calmly, on a Monday, a full two weeks before the event.

What changes when you see the gap 14 days out

The decisions you make shift from "firefighting" mode to "choosing the best option" mode. Those are different financial outcomes.

- You have time to message the client whose receivable went overdue 30 days ago — and get paid before the moment of truth

- You have time to move a conversation with a supplier to another date — without damaging the relationship

- You have time to arrange an overdraft at the planned rate (not an emergency rush rate with a higher percentage)

- You have time to cut non-essential spending — ads, new subscriptions — in advance, rather than after a bad day

One owner put it this way in a consultation: "I used to make decisions at night, when there were no options left. Now I make them in the morning, when there are plenty of options."

If you're already in a cash gap — 7 practical actions

If the panic has already set in and you have to pay tomorrow, here's the sequence of steps. Not general theory, but what actually works.

One. Make a list of all planned expenses for the next 7 days. Rank them by how critical they are: critical (frontline salaries, rent, taxes), secondary (suppliers with flexible terms), non-essential (ads, subscriptions, small stuff).

Two. Call the suppliers in the second category and ask for a 7–14 day deferral. In most cases you'll get a "sure." Especially if you're honest and say — we have a short gap, everything will normalize in two weeks.

Three. Check your receivables. In 8 out of 10 businesses there are clients who are 14–30 days overdue. Call or message each one. Offer a 1–2% discount for payment within 48 hours — this often works.

Four. Approach the bank for a short overdraft. This is a normal tool, not "living on debt." A 14-day overdraft at 25% per annum is 0.96% for the whole period. Cheaper than missing payroll.

Five. Freeze all non-essential spending. Ads, new subscriptions, hiring one more person — pause for a month. It's not forever.

Six. Talk to your team honestly. Not "everything's fine, but…" — rather "we have a short gap, and I can see how to solve it." A team respects honesty more than silence.

Seven. As soon as the crisis is over — set up a payment calendar. Because next time you don't want this same scene to repeat.

How to build a cash reserve for the future

The classic rule is to keep 1–3 months of fixed expenses in the bank. Fixed means payroll, rent, recurring subscriptions. Not variable ones (raw materials, marketing — those adjust to turnover).

For businesses with stable cash flow, 1 month is enough. For service businesses with uneven flow — 2 months. For seasonal ones — 3–6 months, because the difference between high and low season can be 3x.

How to build a reserve if you don't have one right now. Not "set aside 50% of every payment" — that's unrealistic. Redirect profit into the reserve over 6–12 months, until it reaches the target level. That means fewer dividends for the owner now — but far more peace of mind a year from now.

One of our clients — a service business with UAH 200,000/mo in turnover — set aside a UAH 350,000 reserve over 8 months. In the ninth month a crisis hit with a big client who disappeared for 60 days. Without the reserve, this would have been a catastrophic cash gap. With it, just an ordinary working month.

Checklist for this week

If you don't have a payment calendar right now, here's the minimal version of this process you can do in an hour. It won't replace the tool, but it gives you basic visibility.

- Write down all planned expenses for the next 14 days — with specific amounts and dates

- Write down all planned inflows — invoices issued, expected deposits, recurring contracts

- Look at your account balance today

- Build a balance forecast for each day: today + inflows − outflows = tomorrow

- Put a red mark on the days where the balance drops below a safe threshold

- Look at those red days — what can be moved, who you can negotiate with, what to cut

If you manage that, you already have a rough version of a payment calendar in Excel. Not as convenient as a dedicated tool, doesn't update itself — but it already reveals half the picture.

Topic foundation: Cash Flow Gap: How to Identify It and How to Prevent It

Share valuable content — become a source of insights

Frequently asked questions

How is a cash gap different from a loss?

A cash gap is a short-term shortage of money in the till in an otherwise healthy business. It has a specific date and amount ("on June 15 we'll be UAH 1,400 short"). A loss is when expenses consistently exceed income over months. A loss has a trend ("margin has been falling for the last three months"). A cash gap is treated with a payment calendar. A loss is treated by restructuring the business model.

What's the minimum cash reserve to keep?

1–3 months of fixed expenses. For seasonal businesses — 4–6 months. If you don't have this right now, the short-term priority is to see the size of your own fixed expenses, then build the reserve gradually.

Can I keep records in Google Sheets and get by without tools?

Yes, to start with. If you have up to 50 transactions a month and one or two accounts, Sheets will do. You can build a 14–30 day payment calendar with a formula. The problems start when you have 5+ accounts in different banks and currencies, cash, and deposits — keeping the picture up to date in Sheets becomes hard, and the data goes stale within a couple of days.

How do I tell a "short gap" from a "chronic shortage of money"?

One or two gaps a quarter is normal for a business with uneven cash flow. A gap every two weeks is a symptom of a structural problem: either the pricing model is set too low, or controllable costs are too high, or the client base is too dependent on a single client. In that case a payment calendar will only show the scale — what you need to treat is the business model.

Does a payment calendar help seasonal businesses?

Yes, them especially. The calendar can be extended to 3–6 months — and you can see that in February there'll be a UAH 80,000 gap. You have 4 months of lead time — either to build up the cash reserve, or to arrange a credit line with the bank, or to revisit contracts with suppliers.

How long does it take to set up a payment calendar in Finmap?

The basic version — 30–60 minutes. You import 30 days of transactions, set up recurring payments (rent, payroll, subscriptions), and define a minimum cash threshold. After that the system works on its own.

Any questions left?

We are ready to answer them.

Finmap support