Table of Contents

280

5 min

25.06.2026

Financial Management for a Small Business: When You Outgrow Your Own Head

Karine Shevchenko

Financial Expert at Finmap

"For five years I ran the business out of my head. I knew everything. The business was small enough. Then a Tuesday came when I didn't know — and the cost of not knowing showed up that same week."

A founder running a small specialty business — six employees, ₴2.2M revenue, third year of operation — described the moment that ended the "I keep it in my head" approach.

For five years she had managed money the way most small business owners do. Bank balance checked daily on her phone. Bills paid as they arrived. Salaries handled by the accountant. P&L produced quarterly. Mental tracking of who owed her what. It worked. The business was small enough.

Then a Tuesday came. Two clients she'd thought would pay that week didn't. A supplier invoice she'd forgotten was due Wednesday. The accountant called about a tax payment she hadn't accounted for. Salaries were due Friday. None of it was a crisis on its own. All of it together was a crisis — because none of it had been in one place where she could see how it would interact.

She covered the week. Then she sat down to install something the business had outgrown not having: actual financial management.

This article is about that transition — when "small business" is small enough that the owner can carry the finances in her head, when it isn't anymore, and what to install once it isn't.

The Paradox: The Owner's Head Is the Best System Until It Isn't

In the first year of a small business, the owner's head is genuinely the right system for managing finances. There are 2 clients. 1 bank account. 6 monthly subscriptions. The owner knows them all because she set them all up. The overhead of installing a "system" for this level of complexity is greater than the cost of just remembering.

Around year 2–3 of a growing business, this stops being true. Clients hit 8–10. Subscriptions reach 30+. Multiple accounts. Salaries for multiple people. Tax dates. Supplier mix. The mental model that worked at month 6 is increasingly fragile at month 30. The owner doesn't notice until a Tuesday when the gaps connect.

The transition isn't about size in revenue terms. It's about complexity. A ₴1.5M business with 1 retainer client and 1 product line can stay in the owner's head. A ₴1.5M business with 12 clients, 3 service lines, multi-currency, and 4 employees absolutely cannot.

The general framework — what management accounting actually means — is in the anchor article → Management Accounting Explained.

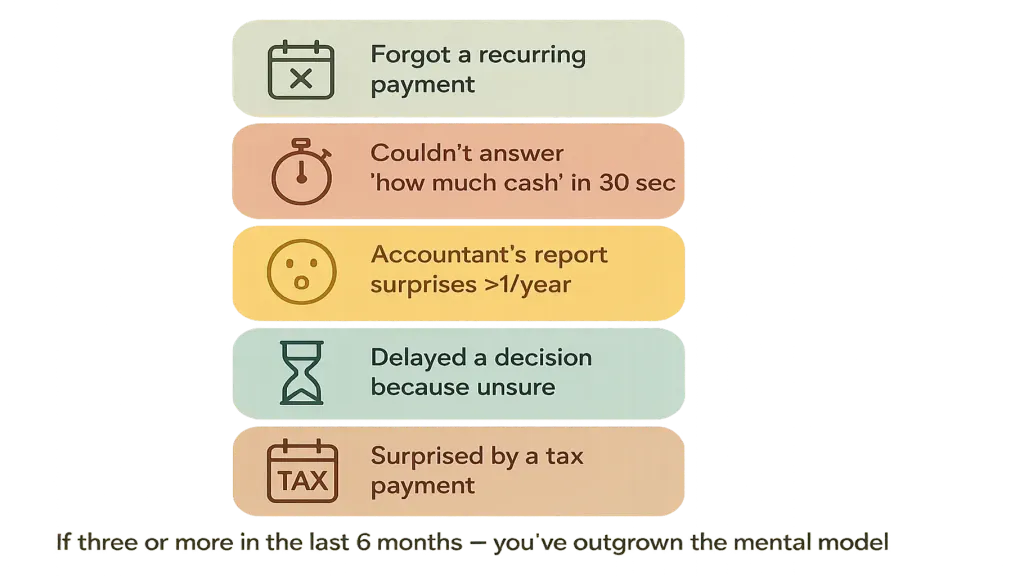

Five Signals You've Outgrown the Mental Model

Two — you couldn't answer "how much cash do we have across all accounts" in 30 seconds. Not within ₴100K. Within ₴10K. If the answer requires opening four apps and adding manually, you're past the threshold.

Three — your accountant's monthly report surprises you in either direction more than once per year. A "we made more than I thought" or "we made less than I thought" surprise reveals that your daily mental model was disconnected from reality. Once a year is normal noise. Quarterly is the signal.

Four — you delayed a decision because you weren't sure of the financial impact. A hire postponed. A piece of equipment debated. A partnership not pursued. These delays are the hidden cost of inadequate financial management — and they accumulate.

Five — you've been surprised by a tax payment in the last 12 months. Tax dates are public, predictable, scheduled by the calendar a year in advance. A surprise here is the canary for the broader financial management gap.

If three or more of these have happened in the last 6 months, you've outgrown the mental model. The Tuesday from the opening is coming, and the question is just when.

What "Financial Management" Means at Small Business Scale

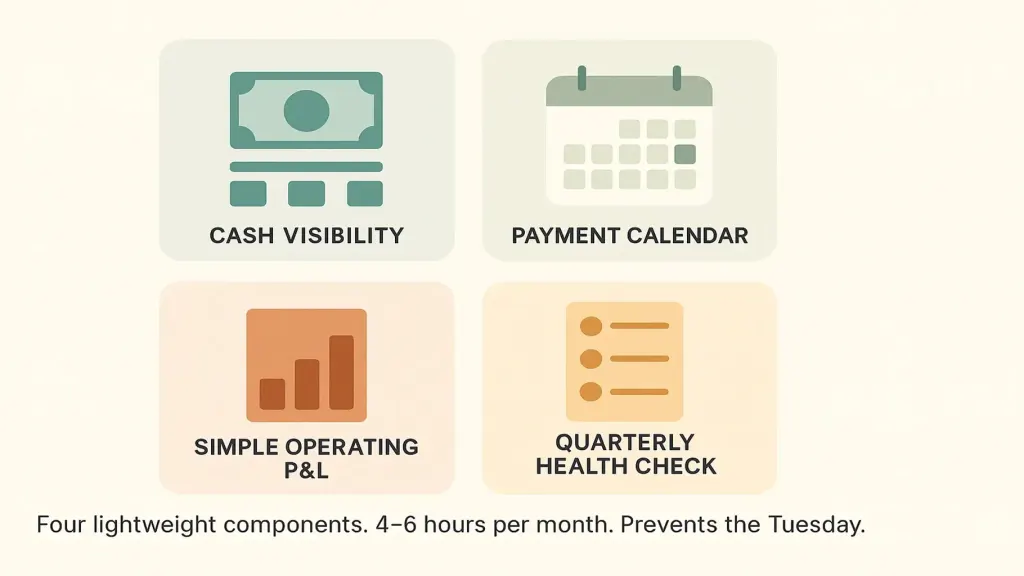

Financial management for a small business doesn't need to be enterprise-grade. It needs to cover four things, lightly but consistently.

Two — payment calendar. A 14- to 30-day forward view of expected inflows and outflows. Tells the owner which days will be tight, which days have slack. Article on payment calendar →

Three — simple operating P&L. Monthly, segmented as much as is useful (by client, by product line, by service). Doesn't need to be elaborate. Just needs to answer "where's our profit actually coming from?"

Four — quarterly health check. Three questions: are we earning more than we're spending and by how much? where's the profit coming from? is anything in our cost structure changing in ways we should respond to? Half an hour, every three months, plus a one-hour annual rebuild.

That's it. Four lightweight components. They take 4–6 hours per month to maintain. They prevent the Tuesday and surface the decisions that grow the business.

How to Install It (the Lightweight 30-Day Plan)

Week 1. Map every account where money lives. Build a consolidated view (spreadsheet or platform). Get to a state where you can answer "how much cash do we have?" in 30 seconds.

Week 2. Build a 30-day payment calendar. List expected inflows (with confidence levels) and committed outflows (with criticality). Spot the tight days. Renegotiate timing where possible.

Week 3. Produce a segmented operating P&L for the previous quarter. By client or by product, whichever is more useful. The numbers will surprise.

Week 4. Set up a 30-minute monthly cadence: 15 minutes updating the calendar, 15 minutes reviewing the P&L. Calendar this for the same time every month.

After 30 days, you have a real management system. The accountant continues their work. You stop carrying it all in your head.

📌 See how lightweight financial management works for a small business — cash visibility, payment calendar, simple operating P&L, quarterly health check — in one integrated view. Book a 20-minute Finmap demo. Book a Finmap demo →

In this topic

- 14 Hours a Week "Checking the Finances" — And Still Surprised

- Outsourced Finance Director: When You Actually Need One

- ₴480K Withdrawn, ₴0 Buffer Left: The Owner Dividend Decision Founders Get Wrong

- ₴100K Revenue, ₴62K in Hand: How to Count Real Profit as a Ukrainian Sole Proprietor

- What Money Management Actually Means in Business (And Why Most Owners Skip Three of the Four Layers)

- The Secret to Profit: How Financial Management Can Help You Earn More

- How to Painlessly Scale Your Business With Cash Flow Management: User-Case of an IT Recruitment Company

Share valuable content — become a source of insights

Frequently Asked Questions

My business is genuinely small (₴500K revenue, solo). Do I need this?

Probably not yet. A simple spreadsheet with monthly income and expenses, plus a weekly bank balance check, covers it. Install the lightweight system when you cross the complexity threshold, not the revenue one.

Should I hire someone to do this for me?

At small business scale, usually no. The act of doing it yourself is what produces the understanding. Hire a bookkeeper for compliance work, but keep the financial management in your own hands until ₴3M+ revenue.

Spreadsheet or platform?

Spreadsheet for the first 6–12 months. Platform when maintenance becomes painful. Article #3 → on platforms

What's the relationship between this and management accounting?

This is the lightweight version of management accounting for small business scale. As the business grows, this practice scales into the full four-artifact framework. Anchor article →

What if I'm already in survival mode and don't have time?

Survival mode is exactly when financial visibility matters most. The 30-day install is itself a survival action — you'll find decisions you didn't know you could make.

My accountant says they handle this. Do they?

Test: ask them to send you the consolidated cash position across all accounts. If they can within 30 seconds, they handle it. If they need a week, they handle bookkeeping, not financial management.

Any questions left?

We are ready to answer them.

Finmap support