Table of Contents

1k

10 min

17.06.2026

₴480K Withdrawn, ₴0 Buffer Left: The Owner Dividend Decision Founders Get Wrong

Sergiy Shuldik

Financial Expert at Finmap

"I took ₴40,000 a month out of the business. That's what felt right. By January I realized: the business had ₴0 in reserve, and I couldn't tell you exactly when that happened."

She runs a small marketing agency. Three years old. Six people on the team. Annual revenue: ₴3,600,000. Net profit margin: 20%. By every external metric, a healthy business.

For all twelve months of the previous year, she had withdrawn ₴40,000 each month as her owner draw. ₴480,000 total. It had felt about right — the business had been steady, clients were paying, no major crises.

The first week of January, doing her annual review, she pulled up the consolidated balance across her business accounts. ₴0 in the strategic reserve. ₴84,000 in the operating account. ₴0 in the tax buffer.

A year before, those numbers had been ₴320K, ₴180K, ₴120K respectively. The business hadn't lost money — net profit had been ₴720K. She had simply taken almost everything out, and a little more.

This is not a story about a bad founder. This is a story about a question almost every owner gets wrong because nobody taught them how to think about it: how much should you actually pay yourself, and when?

The Paradox: Dividends Feel Like Reward, But They're a System

Most founders think about owner dividends emotionally. "I worked hard this month, I deserve it." "Revenue was strong, I can take more." "Things are tight, I'll skip this month." It feels like fair compensation for ownership and effort.

This emotional model is the problem. Dividends are not compensation. They are a financial decision that affects the long-term health of the business as much as any other decision. Taking too much, too fast, or at the wrong time slowly decapitalizes the company — and the owner is usually the last person to notice.

Real dividend discipline is the opposite of emotional. It's scheduled, formulaic, and constrained. The founder doesn't decide each month how much to take — they decide once a year what rules govern withdrawal, and follow them.

The reason this is hard: the bank account doesn't push back. Nothing in your day-to-day operations stops you from taking ₴100,000 this month. The damage shows up six months later, when the buffer that would have absorbed a slow quarter isn't there anymore.

"The cash on hand felt like mine to take. It wasn't. Half of it was already promised to taxes, suppliers, slow months, and growth — I just hadn't separated those buckets."

Owner's Salary vs Dividend — The Line Most Founders Blur

Before talking about how much, we have to separate two different things that most owners mix together.

Owner's salary is the regular monthly pay you take for the work you do running the business. It's an operating expense — a line in the P&L. It exists because if you weren't running this business, someone else would have to be paid to do your work. It's predictable, fixed, and gets paid before profit is even calculated.

Owner dividend is a distribution of profit. It comes after the business has paid all its costs (including your salary), reserved its taxes, funded its growth needs, and topped up its buffer. It's variable, scheduled (typically quarterly), and is what's left when the business is healthy.

The founders who struggle most are those who take a single "owner draw" that mixes both — they pay themselves ₴40K/month and call it operating cost, but mentally treat it as profit-sharing. The result: the business never knows what it actually costs to run, and the owner never knows what real profit exists.

Step one of dividend discipline is drawing this line clearly. Set yourself a monthly salary that's defensibly close to market rate for the work you do. Everything beyond that is a separate decision — the dividend question.

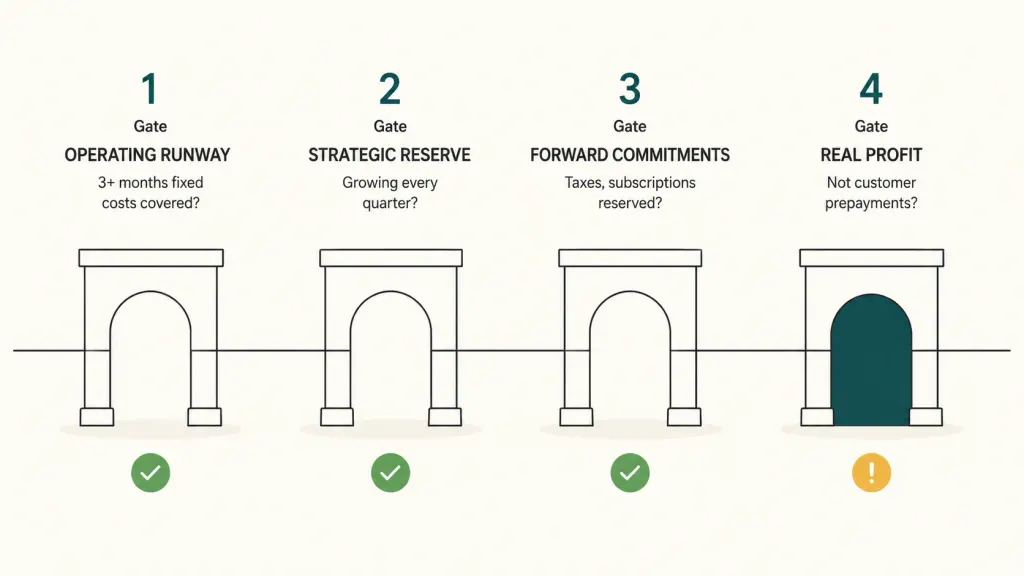

The Four Gates: Questions Before Any Withdrawal

Before you withdraw a single hryvnia of dividend, four gates must all be open. If any one is closed, the answer is "not yet."

Gate 1 — Operating runway. Does the business have at least 3 months of fixed costs in the operating buffer? Fixed costs means rent, salaries (yours included), recurring subscriptions, accountant — the spend that happens whether revenue is strong or weak. If you have less than 3 months covered, no dividend. Top up the buffer first.

Gate 2 — Strategic reserve. Is there a separate strategic reserve growing every quarter? This is the "deep buffer" — money set aside for opportunity (hiring the right person quickly, surviving a major client loss, weathering a 6-month slow stretch). A healthy business adds something to this every quarter, even if small. If it's stagnant or shrinking, the dividend isn't really profit — it's a withdrawal from future safety.

Gate 3 — Forward commitments. Have all known upcoming obligations been reserved? Next quarter's taxes. Annual subscriptions due in 90 days. The new equipment you committed to. The team bonus you promised. If these aren't already segregated in their own buckets, any dividend you take is borrowed against them.

Gate 4 — Real profit, not bank balance. Are you withdrawing from actual profit — money that's truly yours to distribute — or are you withdrawing from cash that's only on the account because customers haven't been billed yet for next month's work? Big difference. A business with ₴500K on the account and ₴400K of unearned revenue (services pre-paid but not delivered) has only ₴100K of real profit.

Only when all four gates are open is the dividend question "yes." The amount question comes next.

The Healthy Dividend Formula

Once the gates are open, the actual math is simpler than most founders think.

Healthy quarterly dividend = (Quarterly net profit − Strategic reserve allocation − Forward commitment top-up) × 60–70%

Two things to notice. First, you only distribute 60–70% of what's available — not 100%. The remaining 30–40% becomes additional operating cushion, slack for unexpected costs, or strategic reserve top-up. This rule alone separates founders who decapitalize their businesses from founders who build durable ones.

Second, the calculation is quarterly, not monthly. A monthly dividend creates two problems: it bleeds the buffer faster than the buffer can replenish from a slow month, and it tempts you to anchor the amount to feel rather than to actual quarterly performance. A quarterly cadence forces you to wait, look at three months of data, and make one informed decision.

For the agency founder in the opening, applying this discipline would have looked like:

- Quarterly net profit (avg): ₴180,000

- Strategic reserve allocation: −₴27,000 (15%)

- Forward commitments top-up: −₴18,000 (10%)

- Available pool: ₴135,000

- Healthy dividend: ₴81,000–₴94,500 per quarter (60–70% of pool)

- Annual dividend total: ₴324,000–₴378,000

Compare that to the ₴480,000 she actually withdrew. The framework would have left her between ₴100,000 and ₴156,000 in the business — enough to rebuild the strategic reserve and never reach ₴0.

5 Mistakes Founders Make With Owner Pay

Across consulting calls with dozens of Ukrainian business owners, the same five patterns repeat.

One. Withdrawing based on bank balance, not on real profit. The bank account shows ₴300K. The owner takes ₴50K. But that ₴300K included ₴80K of customer prepayments for next month's work, ₴40K of taxes due next quarter, and ₴60K that needed to top up the operating buffer. The actual distributable profit was closer to ₴70K — and the ₴50K withdrawal was 70% of it, well above the 60% guideline.

Two. Withdrawing irregularly. "I'll take ₴70K this month because we're flush" creates business unpredictability. The team can't plan. The buffer can't grow steadily. And it teaches the owner that their pay is variable in both directions — which usually means it ratchets up in good months and rarely ratchets down in bad ones.

Three. Withdrawing 100% of profit. The founder thinks "I made ₴200K profit last quarter, so I'll take ₴200K." This leaves zero room for the business to grow, absorb shocks, or invest in next year's revenue. The business stays the same size forever — and the moment something goes wrong, there's nothing to catch the fall.

Four. Forgetting taxes on the withdrawal itself. In Ukraine, dividend distributions have their own tax treatment (typically 5% if specific conditions are met for a corporate structure, or different rates for FOP). Founders who withdraw "₴100K" mentally and only later realize ₴5K–₴18K of that was owed in withholding taxes get into uncomfortable conversations with their accountant in February.

Five. Treating owner's salary and dividend as the same thing. When the line isn't drawn, the business can never honestly answer "are we profitable?" or "what does this business actually cost to run?" Both questions require knowing what the owner's market-rate salary is, separately from profit-share withdrawals.

What the Agency Founder Changed in the Next 12 Months

The conversation with her accountant in January led to a clean restructuring of how she paid herself.

She set a monthly owner's salary at ₴25,000. Defensible market rate for a working agency director — roughly what she'd have to pay an external person to do her role. This became a fixed line in the P&L, treated like any other salary. It removed half the emotional weight from the "how much to take?" question.

She moved to quarterly dividend reviews. First Sunday of each new quarter, 30 minutes with her accountant on a video call. They ran through the four gates, the formula, and a recommended dividend amount. No discussion of "feeling" — just the math.

She capped distribution at 60% of available pool. The remaining 40% rebuilt the strategic reserve and operating buffer over six months.

The first quarter, the formula recommended ₴65,000 in dividend. She had been expecting to take "around ₴120K." Taking the lower number felt strange for a week. By the second quarter — when she could see the buffer rebuilding — it felt obvious.

Year-end results:

- Total withdrawn (salary + dividend): ₴378,000 vs ₴480K the previous year

- Strategic reserve: ₴280,000 (up from ₴0)

- Operating buffer: ₴195,000 (vs ₴84K)

- Net profit: ₴760,000 (slightly higher than previous year, despite "taking less" — because the business invested in two new client acquisitions in Q2 that it couldn't have funded with zero buffer)

She withdrew ₴102,000 less. The business kept ₴391,000 more. She slept noticeably better.

"I thought taking less would feel like a sacrifice. It felt like the opposite — the first time the business actually felt safe."

Topic foundation: Financial Management for a Small Business: When You Outgrow Your Own Head

Share valuable content — become a source of insights

Frequently Asked Questions

Does this framework work for FOPs (Ukrainian sole proprietors)?

Yes — with a wrinkle. As a FOP, the legal distinction between salary and dividend doesn't exist the same way. But the discipline still applies. Treat a portion of your monthly withdrawal as "operating compensation" (planned, fixed) and the quarterly remainder as "profit distribution" (subject to the four gates). The mental separation is what matters, not the legal labels.

What if my business is growing fast — should I take more or less?

Less, almost always. Fast growth is the most cash-hungry phase of a business. You need bigger buffers because variance is bigger. You need to invest in capacity. You need slack for the mistakes that growth uncovers. Founders who grow fast and pay themselves more during the growth phase consistently look back and wish they had reinvested more.

Is 60–70% of available pool a hard rule?

It's a guideline, not a law. Mature businesses with very stable revenue, large existing reserves, and no growth ambitions can responsibly distribute 80–90%. Early-stage businesses with high variance should be closer to 40–50%. The 60–70% range is a healthy default for a 3–7 year old business at steady growth.

Should the owner's salary line on the P&L include taxes?

Yes. The number you pay yourself net is irrelevant for business decisions — what matters is the fully-loaded cost to the business, including any taxes, social contributions, and benefits. Otherwise the business's true cost structure is hidden.

How do I handle multi-founder situations?

Same framework, applied to the combined owner share. If two founders own the business equally and the formula says ₴100K is the healthy quarterly dividend, that's ₴50K each. The four gates apply at the business level, not per founder.

What if I haven't been paying myself a salary at all — just taking owner draws?

Start with the line drawing first. Decide what your monthly salary should be (defensibly close to market rate), make it a formal fixed line. Then look at what's left and apply the framework. If the business can't afford both — that's a profitability problem, not a dividend problem, and dividends should pause entirely until it's resolved.

Any questions left?

We are ready to answer them.

Finmap support