Table of Contents

1.1k

11 min

18.06.2026

14 Hours a Week "Checking the Finances" — And Still Surprised

Sergiy Shuldik

Financial Expert at Finmap

"I had my banking app open more than my email. I knew every supplier payment, every client invoice, every weekly balance — and I still didn't see the ₴280,000 hole that hit us in September."

She runs an IT consulting service business. Six years old. Twelve people. Annual revenue: ₴6,000,000. By external measures, a successful firm with a steady book of clients.

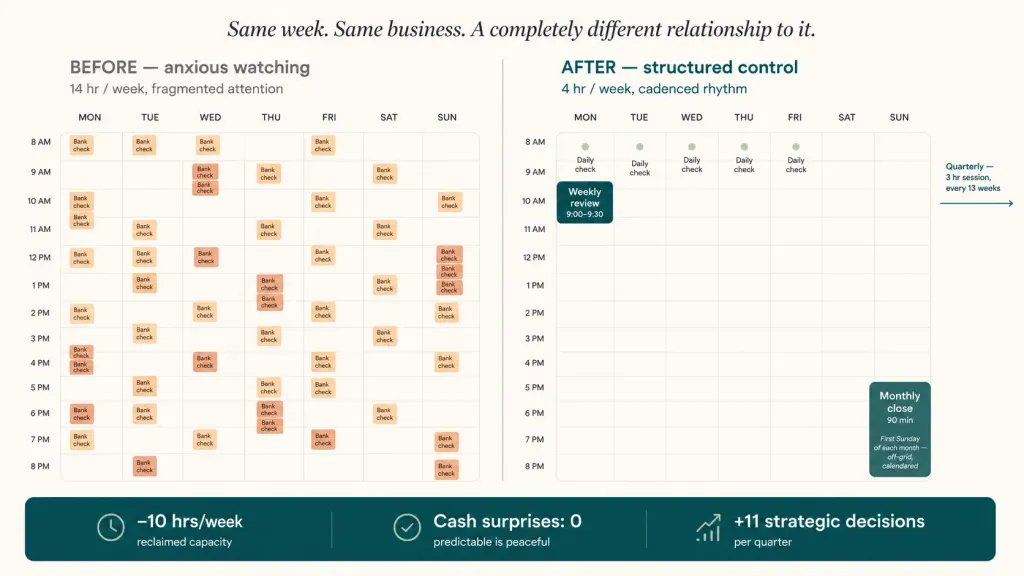

She also spends, by her own count, roughly two hours every day on financial monitoring. Bank apps in the morning. Spreadsheet review at lunch. Quick cash glance before bed. Mental simulations on the weekend. Total: about 14 hours a week — almost a part-time job — devoted to "watching the finances."

And in late September of last year, she missed a ₴280,000 cash shortfall by a full 30 days. A single large client delayed payment by 6 weeks. Two new deals slipped from August to October. ЄСВ payments came due. The combination should have been visible by mid-July. But her 14 hours a week were spent watching, not controlling — and the difference between those two words is most of this article.

The paradox is uncomfortable. More hours spent on finances do not equal more control. Often they equal more anxiety with less actionable signal. This is the story of what changed when she replaced anxious watching with a real system — and got back 50+ hours a month in the process.

The Paradox: Watching Is Not Controlling

Most founders, when their business gets large enough to feel financially complex, develop a habit they call "keeping a close eye on the finances." In practice, this habit is:

- Opening the banking app multiple times a day

- Mentally running cash simulations during the commute

- Glancing at the latest P&L the moment the accountant sends it

- Pulling up the spreadsheet whenever a client pays or a supplier sends an invoice

- Lying awake some nights estimating next month

This is not control. This is anxious monitoring. It produces stress, eats hours, and provides little useful signal — because the data being watched (today's bank balance, this week's incoming payment) is mostly noise, while the signals that actually matter (90-day cash forecast, contribution margin by client, fixed cost trajectory) are not even on the screen.

"The thing I was watching was the wrong thing. Cash on hand today doesn't tell you about October. By the time the bank balance shows a problem, the problem has been there for weeks."

Real financial control is structurally different from anxious watching. It has cadences. It has clear decision rights. It has defined signals. And — counterintuitively — it takes much less time, because each unit of time is spent on the right question, not on whatever question is causing anxiety in that moment.

This article is about how to install it.

The Four-Cadence Control Loop

Financial control is not one activity. It's four activities at four different cadences, each with a different purpose, each with a different time investment. Together they form a control loop that catches problems 30–90 days before they arrive.

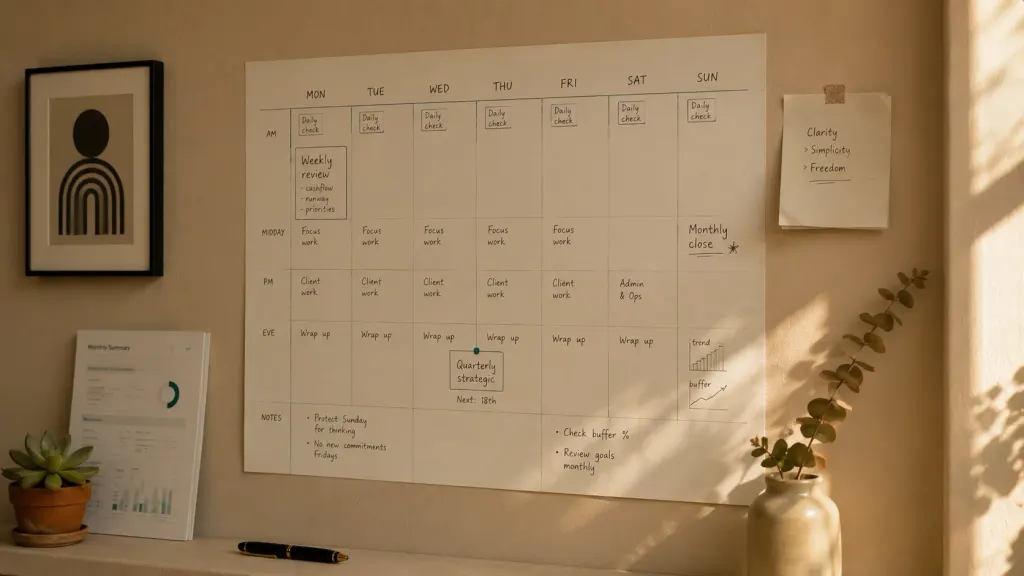

Daily — 5 minutes — "Are we operationally safe today?"

The only legitimate daily question is whether anything anomalous happened in the last 24 hours. A glance at the consolidated cash position. A scan of any unusual transactions. That's it. Anything more than 5 minutes a day on finances is anxiety, not control.

Weekly — 30 minutes — "Are we on track this week?"

Once a week, ideally Monday morning, look at the 14-day payment calendar. Are there client payments expected this week that haven't arrived? Are there supplier payments due? Is anything you committed to last week now problematic? This catches issues 1–2 weeks before they become critical.

Monthly — 90 minutes — "What does last month tell us?"

First Sunday or Monday of each month, a 90-minute structured review. Full P&L for the closed month. Variance vs forecast — what was budgeted, what actually happened, why the gap. Refresh the 90-day cash forecast based on this month's reality. Update key metrics: contribution margin per client, fixed cost trajectory, runway in months.

Quarterly — 3 hours — "Are we on the right strategic path?"

Once a quarter, a half-day session — ideally with the accountant or a financial advisor. The big questions: Is the seasonal pattern still what we think? Should pricing change? Should headcount change? Is the dividend formula still appropriate? Are there structural shifts in client mix, costs, margins? This is the layer where real strategic decisions get made.

Total time investment: about 4 hours per week — including the daily glances. Less than a third of what anxious watching consumes. With dramatically more useful output.

The Decision Rights Matrix — Who Decides What

The second leg of real control is clarity about who decides what at what threshold. Most founders default to "I decide everything" — which sounds responsible but is actually the opposite of control. It creates bottlenecks. It means small decisions get the same scrutiny as large ones. It guarantees that the founder is in the weeds when they should be doing strategic work.

A working decision rights matrix for a ₴3–10M Ukrainian service business looks something like this:

| Decision type | Founder | Ops Manager | Accountant | Advisor |

|---|---|---|---|---|

| Strategic direction, pricing, market | Decides | Informed | Informed | Advises |

| Hires > ₴50K monthly cost | Decides | Advises | Informed | – |

| Hires < ₴50K monthly cost | Approves | Decides | – | – |

| Spending < ₴30K, recurring or one-off | Informed | Decides | – | – |

| Spending ₴30K–₴100K | Approves | Proposes | Reviews | – |

| Spending > ₴100K | Decides | Proposes | Reviews | Advises |

| Tax compliance, reporting | Informed | – | Decides | – |

| Owner draws and dividends | Decides | – | Reviews | Advises |

| Day-to-day operations | – | Decides | – | – |

The exact thresholds matter less than the principle. Each decision type has one person who "decides" — single point of accountability — and others who approve, are informed, or advise. No decision is owned by no one. No decision is owned by everyone.

Once this matrix exists, "watching the finances" stops being a continuous founder activity and becomes a series of structured moments. The 5-minute daily glance answers "anything unusual?" The 30-minute weekly review answers "anything in the next 14 days that needs my decision?" Most days, the answers are "no" and "nothing" — and the founder gets back to building the business.

The Four Anti-Patterns of Anxious Control

Across consulting calls with dozens of Ukrainian business owners, the same four anti-patterns repeat. The IT consulting founder had committed all four.

Anti-pattern one. The daily bank balance check. Opening the banking app multiple times a day to "see where we are." This activity costs hours per week and produces almost zero useful signal — because daily fluctuations are mostly noise. The only legitimate daily question is "anything anomalous?" — and that requires 90 seconds, not 90 minutes.

Anti-pattern two. The single-bucket P&L review. Looking at a monolithic profit-and-loss number and feeling reassured (or alarmed) without segmentation. Real review requires breaking down: by client, by service line, by month, by cost category. The aggregate number can be healthy while the underlying mix is rotting. Anti-pattern is to never look at the components.

Anti-pattern three. The "I'll review when there's time" trap. Pushing monthly and quarterly reviews to "when things calm down." They never calm down — that's the nature of running a business. The monthly review needs to be a calendar event with a fixed slot, like a payroll cycle. Skipping it once means skipping it three times in a row, and then noticing six months later that something major has shifted.

Anti-pattern four. The "everything is a founder decision" trap. Refusing to delegate any spending or operational decision because "what if it's wrong?" The result is the founder spending hours per week on ₴2,000 decisions, while the ₴200,000 strategic decisions get less attention than they need. The fix is the decision rights matrix — owned consistently, not improvised.

These four patterns are why founders can spend 14 hours a week on finance and still be surprised. The activities feel productive but aren't producing control.

What the Consulting Business Changed in 90 Days

After the September shortfall — which she covered by drawing on a personal line of credit at uncomfortable interest — the founder made three changes.

She installed the four-cadence loop. Daily 5-minute glance at 8:30 AM, before checking email. Weekly 30-minute review every Monday morning. Monthly 90-minute close on the first Sunday of each month, with her accountant joining for 30 minutes of the 90. Quarterly 3-hour session with both the accountant and an external financial advisor. The cadences became calendar events with their own meeting blocks — non-negotiable, not movable for "urgent" matters.

She built the decision rights matrix with the operations manager. Spending decisions under ₴30K moved entirely to the ops manager. Hiring decisions under ₴50K monthly cost: ops manager decides, founder approves. Above those thresholds, founder decides. The matrix lived on a printed page on her desk and on a Notion page the team could reference.

She stopped opening the banking app outside of cadenced moments. A specific banned-behavior rule. The app on her phone got moved to a folder she didn't visit. The 8:30 AM check was the only time she looked. When the anxiety urge hit — and it did, often, for the first three weeks — she noted it on a list of "things to discuss at the Monday weekly review."

Twelve weeks later:

- Time spent on finances per week: dropped from ~14 hours to ~4 hours (the cadenced time only)

- Anxiety-checks per day: dropped from 6+ to 0 by week 5

- Strategic decisions actually made: 11 in the first quarter, vs. 4 the prior quarter (because they were no longer being crowded out by tactical micro-decisions)

- Cash surprises: zero. The October-November pipeline soft spot was spotted in mid-August and managed proactively (early-pay discount on three invoices, postponed two equipment purchases, kept the credit line untouched).

- Net profit: roughly flat for the quarter (∼₴380K) — the impact of the system shows up over multiple quarters, not in 12 weeks. But the 50+ hours per month she got back went into landing two new clients in Q4 that grew the business 18% YoY.

"The amazing thing wasn't that I had more control. It was that I had more control while doing less of what I was doing before. Anxiety isn't control. It's just anxiety with a finance label on it."

Topic foundation: Financial Management for a Small Business: When You Outgrow Your Own Head

Share valuable content — become a source of insights

Frequently Asked Questions

How do I get started if I'm currently in the "anxious watching" pattern?

Start with the daily 5-minute rule, plus a banned-behavior rule for the banking app outside of that window. Just those two changes for two weeks. They produce immediate stress relief and demonstrate that nothing breaks. Then add the weekly 30-minute review. Build to monthly and quarterly over a quarter.

Do I need a financial advisor for the quarterly review?

Strongly recommended for businesses above ₴3M annual revenue. An external advisor at the quarterly cadence — someone who sees many businesses, can benchmark, and isn't anxious about your specific situation — adds perspective that an inside-the-business view misses. For smaller businesses, the founder + accountant combination can substitute, but the founder must commit to genuinely strategic questions, not operational ones.

What if my operations manager isn't ready to own ₴30K spending decisions?

Lower the threshold initially. Start at ₴10K, watch how decisions are made for a month, then raise. The point is the structure, not the specific number. A clear ₴5K decision threshold owned by someone other than the founder is better than no threshold at all.

Can the decision rights matrix change?

Yes, intentionally — typically reviewed at quarterly cadence. Avoid changing it ad-hoc in the middle of a quarter, which destroys its trust and predictability. Treat it like a constitutional document — stable, occasionally amended through deliberate process.

What if a problem appears outside the cadence — do I just wait?

Real problems still get addressed when they arise. The cadence isn't about ignoring fires; it's about not creating fires through anxious watching. If something genuinely urgent surfaces — a major client lost, an unexpected ₴500K invoice — you act. But ₴1,200 in unexpected hosting fees is not urgent; it goes into the weekly review queue.

How long does it take to feel real?

For most founders: the daily anxiety drop happens in week 2. The "I trust the system" feeling lands around week 6. The quantitative results — better decisions, fewer surprises, more strategic time — become visible by quarter two. The system gets stronger every quarter as the data underneath it gets richer.

Any questions left?

We are ready to answer them.

Finmap support