Table of Contents

407

5 min

09.07.2026

30-Day Cash Forecast: How a Small Business Owner Sees the Next Month Before It Happens

Oleksandr Solovei

CEO & Co-founder Finmap

30-Day Cash Forecast: How a Small Business Owner Sees the Next Month Before It Happens

"On the 22nd of every month I asked myself the same question: will there be enough for salaries on the 5th? Some months I knew. Most months I hoped. Hope is not a financial plan."

There's one question every small business owner in Ukraine returns to, over and over, month after month: will there be enough cash when the salaries are due? On paper the answer usually is. In the bank account, the answer is a different story — because payments arrive late, taxes fall unexpectedly, one client pauses, one supplier prepays.

Most owners answer this question with a mix of memory, hope, and mental arithmetic. It works most of the time. When it fails, it fails at the worst possible moment.

A 30-day cash forecast — a real one, not a guess — changes that. Not by predicting the future perfectly, but by making the shape of the next 30 days visible enough that surprises stop being surprises.

Why Cash Feels Unpredictable (Even When It Isn't)

One — inflows arrive on schedules you don't set. You issue an invoice on the 1st. The client pays on the 25th. Some pay on the 40th. Averaged across 8 clients, "when the cash arrives" becomes a fog even when each individual client is predictable.

Two — outflows are more scheduled than you notice. Rent, salaries, tax, top suppliers, subscriptions — most of your outflows are calendar-locked. You already know when 70–80% of the month's money will leave. You just haven't written it down.

Three — memory smooths the edges. Your mental picture of "usual" hides the days that are tight. The 22nd feels like a normal day; the 4th feels like payroll day. But your bank runs continuously — every day matters.

Four — you're missing the visualisation. A list of numbers isn't a forecast. A line that starts where you are and ends 30 days later, with the tight days visibly darker, is.

How to Recognise You Need This

- You've been surprised by a tight day in the last three months.

- Your standard answer to "will we have money for X?" is "I think so".

- You take out short-term credit to cover routine gaps that were predictable.

- Your accountant closes the month but nobody predicts the next one.

- You've said "все в Excel, але щось не вношу, забуваю" ("it's all in Excel but I don't always enter things — I forget").

How to Solve It — The Four-Layer 30-Day Forecast

Set aside 90 minutes. Bank statement export, invoice list, calendar of committed payments, one spreadsheet or your finance platform.

Layer 1 — Starting cash across all accounts.

Consolidated balance today. Sum of every account, every currency converted to UAH at today's rate. This is the point where the line starts.

Layer 2 — Committed outflows, day by day.

Rent (usually 1st or 5th). Salaries (usually 5th or 15th). Tax obligations (their fixed calendar). Top 5 suppliers by expected due dates. Subscriptions renewing. Loan repayments. Every one placed on its exact day.

Layer 3 — Expected inflows, with confidence.

Every open invoice with the expected payment date and a confidence tag (high / medium / low). "High" if the client is reliable and confirmed the date; "medium" if the invoice is fresh but the client is on time historically; "low" if the client has been slow.

Layer 4 — Running balance, day by day.

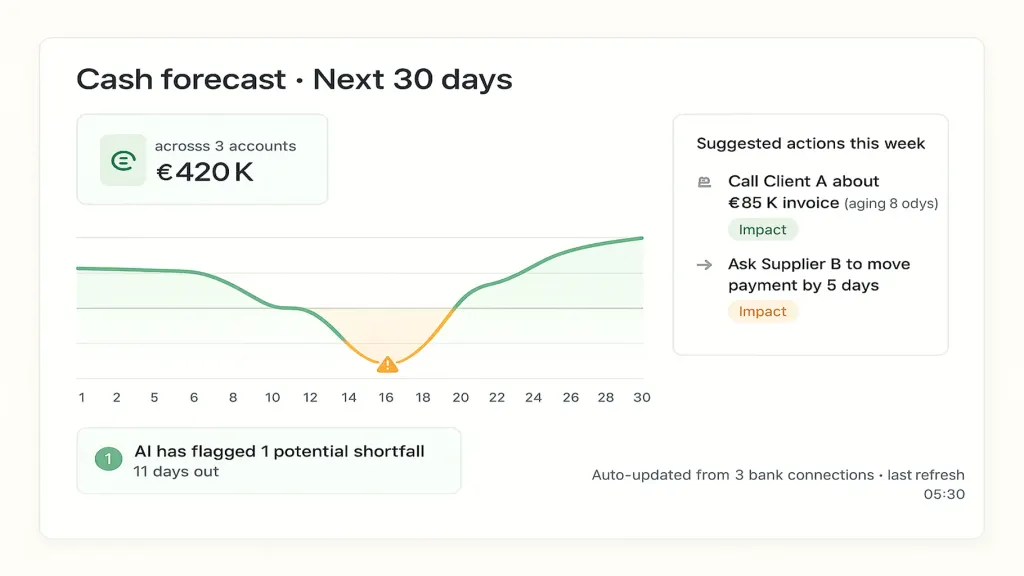

Starting cash plus each day's expected inflows minus each day's outflows = tomorrow's balance. Tomorrow's balance is the day after's starting point. The line runs for 30 days.

Days where the running balance crosses below a comfortable buffer (typically two weeks of fixed costs) show as amber. Days below zero show as coral. The rest is green.

This is not a prediction. It's a projection. As reality unfolds and payments arrive earlier or later than expected, you update the layer and the line reshapes. The value isn't in perfect accuracy — it's in seeing the shape a week or two before the day arrives.

What Changes When You Actually Have This

Three quiet outcomes over the first month of running the forecast weekly.

One — you catch tight days 10–14 days in advance. With that runway, you can call a slow-paying client, offer a small early-payment discount, or reschedule one supplier — and the tight day becomes a normal day.

Two — you stop taking short-term credit for predictable gaps. Because they were only surprises, not shortages.

Three — the Sunday-night anxiety drops. The 22nd is no longer the day you start guessing about the 5th. You already know.

Where the Math Comes From (and Where AI Adds to It)

The forecast starts as arithmetic — inflows in, outflows out, running balance. Any owner can build the first version on a spreadsheet in 90 minutes.

At scale — 3+ bank accounts, dozens of open invoices, seasonal supplier patterns, multiple currencies — the arithmetic is still simple but the maintenance is heavy. Every payment received needs to reset the line. Every new invoice moves the forecast. Every currency shift shifts the balance.

This is where a modern finance platform helps. Finmap connects directly to your banks, watches invoices arrive and clear, notices supplier patterns from your history, and rebuilds the 30-day forecast every time something changes. The line stays accurate without you touching it — you look at it, not maintain it.

The AI layer adds the next step: it watches the forecast for you between your reviews. When it detects a tight day forming 10 days out that wasn't visible before, it flags it. When a client's payment behaviour shifts and their confidence tag should change, it suggests the update. Not because AI is the point — because it's the mechanism that keeps the forecast trustworthy without adding a job to your week.

The Numbers Behind Finmap

- 18,000 business clients in 54 countries use the platform.

- 97% of clients stay with Finmap for years — retention as evidence the tool actually delivers.

- PMF signal: 56% of users would be "very disappointed" if Finmap disappeared (the industry benchmark for product-market fit is 40%).

The 30-day cash forecast is one of the five core things Finmap owners rely on daily.

Three Mistakes Small Business Owners Make

- Forecasting cash flow only monthly. A month is too coarse. Tight days don't announce themselves in monthly totals.

- Skipping confidence tags on inflows. Every optimistic forecast comes from treating "expected" as "confirmed". Confidence tags are what keep the line honest.

- Building the forecast once and letting it drift. A forecast that isn't updated weekly is worse than no forecast, because it looks authoritative while being wrong.

📌 See your 30-day cash forecast auto-built from your banks and invoices, updated in real time, with tight days flagged before they arrive. Free for 14 days, no card required.

Start your free 14-day Finmap trial → finmap.online/ua

Знаєш що зараз. Бачиш що буде. Знаєш що робити.

Topic foundation: Cash Flow Management for a Small Business: How to Always Know Where Your Money Is

Share valuable content — become a source of insights