Table of Contents

695

5 min

07.07.2026

Dividends from a TOV vs Draws from a FOP: The Real Cost of Getting Your Own Money Out

Oleksandr Solovei

CEO & Co-founder Finmap

"For years I ran a TOV because I'd been told it was 'more serious'. Then I ran the math on what it actually cost me to take money out compared to a FOP structure. It wasn't a small number."

Somewhere between year two and year four, most Ukrainian small business owners have the same conversation with an accountant, a spouse, or themselves: is my legal structure the right one for how I'm actually running my life and business?

The framing usually reduces to a shorter question: how much does it cost me, in real terms, to take profit out? A TOV dividend feels prestigious; a FOP draw feels casual. The tax and fee comparison, once you put it on paper, tells a story most owners haven't run the numbers on.

This article is that comparison — with worked examples in current Ukrainian rules — and the decision framework for choosing between structures.

Why This Problem Occurs

One — legal structure was chosen for a reason that no longer applies. Many TOVs were set up because "we might need investors" or "clients demand it". Both conditions may have changed since.

Two — the withdrawal cost is invisible until you calculate it. Corporate profit tax + dividend tax stacks in a way that's not obvious from either rate individually.

Three — the FOP simplified system is more flexible than owners realise. For most owner-operator businesses under ₴8M revenue, FOP на 3-й групі (5%) is remarkably efficient. For those over the FOP threshold, the choice is more genuinely nuanced.

Four — nobody teaches this comparison because it's specific to Ukrainian rules. International SMB content skips it entirely; Ukrainian tax articles cover mechanics but rarely the owner's cost math.

How to Recognise You Need This Analysis

- You're on a TOV structure and haven't recalculated the effective withdrawal cost in the last two years.

- You're on a FOP structure but revenue is approaching or exceeding the group threshold.

- You mix a TOV and a FOP in the same personal finance and don't have a written policy for which pays you.

- You feel like your legal structure and your actual business shape have drifted apart.

How to Solve It — The Cost Comparison and Decision

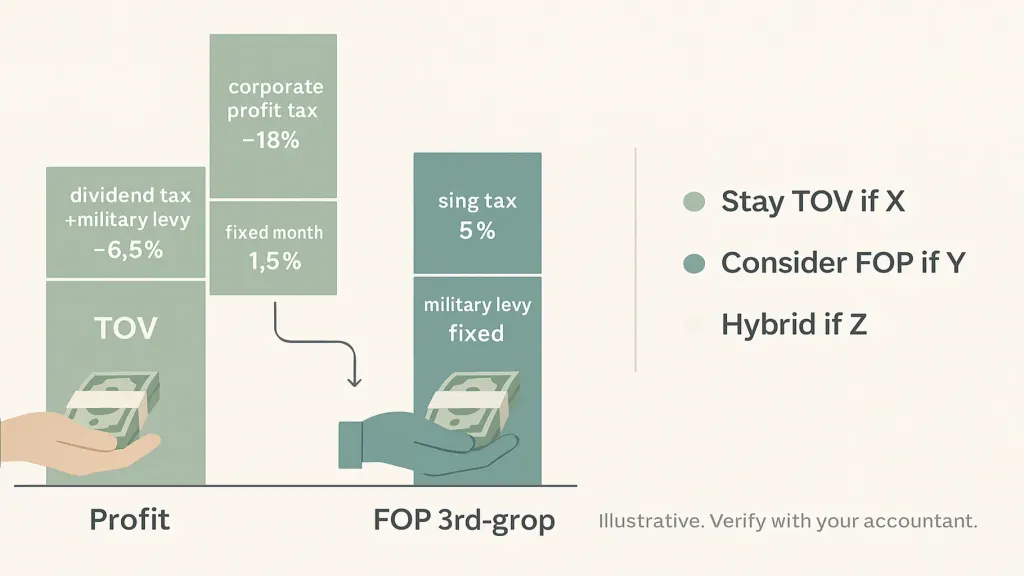

The math on ₴500K annual profit (illustrative, current rules apply)

TOV path (simplified illustration, verify with your accountant for your specific situation):

- Corporate profit tax on the ₴500K profit: ~18% = ₴90K

- Remaining ₴410K distributed as dividend

- Personal dividend tax + military levy on the dividend: ~6.5–9.5% depending on classification

- Net into the owner's hand: roughly ₴370–₴385K — an effective withdrawal cost of ~23–26%

FOP path on 3rd group simplified (5%), illustrative:

- 5% single tax on ₴500K revenue (assuming this profit was booked as revenue): ₴25K

- Military levy on the same base: ~1.5% = ₴7.5K

- Unified social contribution (ЄСВ), fixed monthly: roughly ₴17K annually

- Owner's hand: ₴450K+ — effective withdrawal cost around 10%

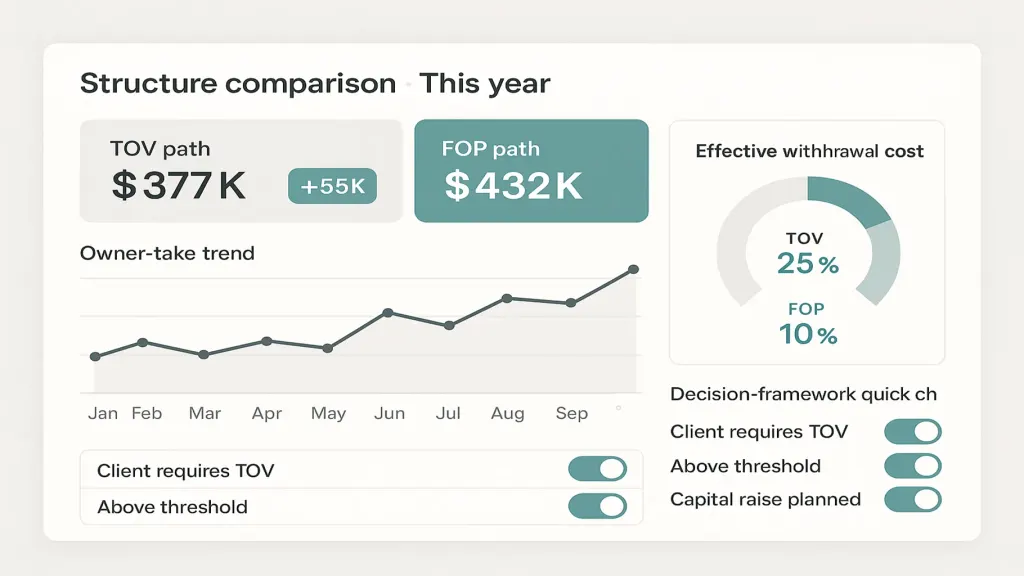

The gap in this simplified example is 13–16 percentage points on the same profit. On ₴500K, that's ₴65–₴80K per year. On ₴2M profit, it's ₴260–₴320K per year.

Important caveats:

- These are illustrative numbers. Actual amounts depend on FOP group, whether profit equals revenue, exact rates, and non-tax factors.

- Some situations legitimately require TOV (large B2B contracts, investors, foreign clients with specific requirements).

- FOP has group thresholds — the 3rd group has a revenue cap (currently around ₴8M). Above that you exit the simplified system.

Consult your accountant before restructuring. The decision framework below is the analysis; the numbers are your own.

The decision framework

Stay TOV if:

- You genuinely need TOV status for client contracts or investor arrangements

- Revenue is well above FOP thresholds and structural

- You're planning to raise capital or sell in the next 24 months

- Multiple owners already own share

Consider FOP (or hybrid) if:

- Single owner-operator, under FOP threshold

- Clients don't require TOV

- No investor or exit plans in near term

- The withdrawal cost math shows meaningful savings that would fund reserves, hiring, or personal life

Hybrid (TOV + FOP together) works when:

- Different revenue streams have different structures naturally (services under FOP, product line under TOV)

- Written policy governs which entity pays the owner what

A platform like Finmap can track TOV and FOP entities separately with a consolidated owner-take view — so the total effective withdrawal cost surfaces monthly, not just at year end.

What Changes When You Actually Do the Analysis

Three quiet outcomes are typical.

One — some TOV owners restructure. They discover the TOV was set up for a condition that no longer applies and the withdrawal cost is meaningful. Restructuring takes months and has one-off costs; the annual savings often justify it.

Two — some FOP owners tighten discipline. The math surfaces that their choice is efficient — but only if the simplified accounting is done cleanly. Confusion between business and personal cash undoes the tax advantage.

Three — hybrid owners get a written rule. No longer "whatever's convenient" — a clear policy that survives the year.

The Written Owner-Take Policy

Regardless of structure, write down (once, for the year):

- Which entity pays the owner

- Fixed monthly amount (owner's salary equivalent)

- Rules for extra draws (frequency, trigger, memo)

- Annual settlement — when the total is reconciled with tax planning

Three Common Mistakes

- Comparing marginal rates only, not stacked effective rates. The corporate + dividend stack tells the real story.

- Forgetting non-tax friction. Bank fees, accounting cost per structure, time cost of compliance. Add these to the tax comparison.

- Doing the analysis once and never revisiting. Rules change; revenue changes; the right structure changes. Review every 24 months.

📌 See TOV, FOP, and owner-take side by side in one integrated view — so the effective withdrawal cost is visible monthly, not just at year end. Book a 20-minute Finmap demo → finmap.online/ua

Read also

Share valuable content — become a source of insights

Frequently Asked Questions

Are these numbers exact?

No. Illustrative. Your accountant produces the exact numbers for your situation and jurisdiction.

Should I switch structures?

Only after analysis with your accountant. Structural change has one-off costs (registration, banking, contract amendments) that must be weighed against ongoing savings.

Can I run both structures at once?

Yes, if there's a genuine business reason (different revenue streams). Written policy required.

What about the FOP group thresholds?

Groups have revenue caps and activity restrictions. If you approach the threshold, plan the transition in advance.

Does this apply if I have foreign clients?

Currency and reporting add layers. Consult your accountant for foreign-currency contract treatment.

Any questions left?

We are ready to answer them.

Finmap support